This is the County Auditor's Office's 2024 Financial Condition Report for Multnomah County Oregon.

Executive summary

This report provides a useful look back at historical trends, which include the impact and recovery from the Great Recession of 2008/2009 and from the COVID-19 pandemic. This data can help inform future decision making.

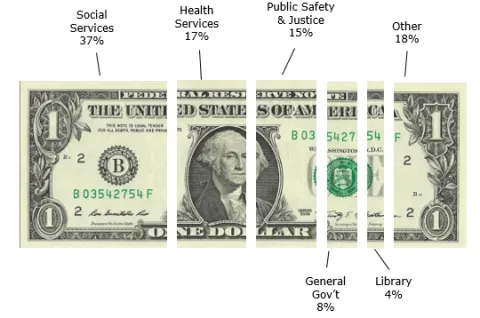

Expenditures by Program in FY2023

Total Expenditures = $2,192,213,000

Social Services continue to be the largest expenditure by program.

As shown in the chart above, the percentage of total expenditures to each area was:

- Social services 37%

- Health services 17%

- Public safety & justice 15%

- General government 8%

- Library 4%

- Other 18%

FY2023 highlights

- Metro Supportive Housing Services intergovernmental revenues of about $146 million

- Preschool for All tax revenues of about $199 million

Visit the dashboards that detail the county's financial condition.

Revenues increased over 93% from Fiscal Year 2010 (FY10) to FY23, adjusted for inflation. The change is the result of steady economic recovery after the Great Recession, federal and state funding support during the pandemic, as well as new revenue sources from two different voter approved taxes: Preschool for All and Metro Supportive Housing Services.

Expenditures increased over 73% from FY10 to FY23, adjusted for inflation. The change is the result of the county responding to the changes in revenues.

A note about the dashboards: We express all indicators in constant dollars with the option to turn off the inflation adjustment. These adjustments for inflation convert dollar amounts to the equivalent of the purchasing power of money in the fiscal year ending June 30, 2023 (or calendar year ending December 31, 2023 where applicable). The adjustments are based on the CPI-W West - Size A, Consumer Price Index (fiscal year average = second half to first half), and index that measures price changes on a quarterly and annual basis.

Yearly fiscal highlights

Below are some significant fiscal highlights that have impacted the county since 2014.

FY2023

- Increase in revenues (over $12 million) and expenditures (over $6.5 million) related to the Preschool for All Program fund.

- Metro Supportive Housing Services (MSHS) intergovernmental revenues for housing services increased by more than $45.8 million over the prior year. There was also an increase of over $47 million in the Supportive Housing fund which accounts for expenditures for supportive housing for those people experiencing or at risk of homelessness.

- These increases are off-set by a decrease in the COVID-19 special revenue fund for intergovernmental revenues of almost $33 million from the prior year.

FY2022

- The new Metro Supportive Housing Services (MSHS) business income and personal income tax was approved by voters in 2020 and became effective January 1, 2021. In FY2022, Metro provided over $97.8 million MSHS intergovernmental revenues to the county for housing services.

- The Preschool for All Program fund was new in FY2022. The new Multnomah County Preschool for All (PFA) tax was approved by the voters in 2020 and became effective January 1, 2021. The voter-approved ballot measure established a new and permanent personal income tax within Multnomah County to fund universal, tuition-free, voluntary, and high-quality preschool education for every three and four-year-old residing within Multnomah County. Tax collections totaled $187 million in FY2022.

- Construction costs related to the Behavioral Health Resource Center (BHRC) project. The BHRC facility has been programmed to provide peer support services, offer transitional housing for homeless people with behavioral health issues, and assist people with finding housing and treatment services.

- The Multnomah County Library Capital Construction Project for planning, renovation, and construction of certain library facilities as approved by Multnomah County voters on November 3, 2020, as Ballot Measure 26-211.

- Business Income Tax (BIT) increased by over $33 million. BIT collections had one of the largest year-over-year increases in the last three decades. The increase is due to a record level of corporate profits as the economy rebounds from the pandemic.

- Motor vehicle rental tax & the Special Excise Tax increases from FY21 to FY22 are also a reflection of the economic recovery after the effects the COVID-19 pandemic had on travel and tourism.

- Newly created Health Department FQHC Fund. The fund was created to separate the activities for Federally Qualified Health Centers (FQHC). Balances for the activities that were previously reported in the General Fund and the Federal/State Program Fund were transferred into this new fund in order to capture all activities related to FQHC within this fund.

FY2021

- The new downtown courthouse opened in October 2020.

- Over $156.8 million in intergovernmental revenues recognized related to the COVID-19 pandemic.

- A $32 million (31%) increase in the business income tax (BIT) due to a couple of factors:

- The Board of County Commissioners approved a tax rate increase from 1.45% to 2.0% beginning with tax year 2020.

- The federal aid provided over the last two years to help address the impact of the pandemic increased overall incomes, boosting increased spending and aggregate demand. This resulted in some of the largest payers of the County's BIT having stronger than expected profits coming out of the pandemic.

- General Obligation bonds issued to finance capital costs to expand, modernize, rebuild, and acquire land for library facilities.

FY2020

- An emergency declaration for the COVID-19 pandemic was declared in March 2020.

- The Behavioral Health Managed Care Fund program transitioned to Health Share Oregon (HSO). Beginning January 1, 2020, the Health Department was no longer operating as the Multnomah Mental Health (MMH) Risk-Accepting Entity as part of HSO.

FY2019

- The new Health Department headquarters opened.

- The county went live with a new suite of enterprise resource planning (ERP) systems in January 2019.

- Significant projects under construction included the central courthouse.

FY2018

- The county's new ERP system replacement project was under way in FY2018.

- Wapato facility was sold in FY2018.

- Significant projects under construction included the downtown courthouse and the Health Department headquarters.

FY2017

- In 2016, Multnomah County and the City of Portland created the Joint Office of Homeless Services (JOHS), thereby consolidating homeless services under the county. Beginning in FY17 the county began recognizing funding related to the JOHS program.

- $25 million lump sum annual payment (at the discretion of the county's CFO) to PERS starting with FY2017 per Resolution 2016-1.7.

- Significant projects under construction included the downtown courthouse and the Health Department headquarters.

FY2016

- At the beginning of FY2016 the Department of County Human Services (Social Services) transferred Mental Health and Addictions Services (MHAS) to the Health Department (Health Services).

- The Sellwood Bridge project was completed and the new bridge opened in the spring of 2016.

- The downtown courthouse construction project began the design and construction phase.

FY2015

- The City of Portland contributed $20 million to the Sellwood Bridge project.

FY2014

- About $75 million received for the Sellwood Bridge construction project. Two-thirds of the $75 million came from the City of Portland, about $20 million came from federal awards, and about $5 million came from direct state funding.

- The county received $10 million from the Portland Development Commission as an initial payment for the construction of a new downtown Health Department headquarters.

Objectives, scope, & methodology

The objective of this report is to evaluate the financial condition of Multnomah County using the Financial Trend Monitoring System developed by the International City/County Management Association (ICMA) and the indicators suggested by the Government Accounting Standards Board (GASB).

We express all indicators in constant dollars with the option to turn off the inflation adjustment. These adjustments for inflation convert dollar amounts to the equivalent of the purchasing power of money in the fiscal year ending June 30, 2023 (or calendar year ending December 31, 2023 where applicable). The adjustments are based on the CPI-W West - Size A, Consumer Price Index (fiscal year average = second half to first half), and index that measures price changes on a quarterly and annual basis.

Throughout this report, we have included the state payments to intellectual and developmental disabilities (I/DD) service providers. In FY08, the state began paying community service providers directly, where in prior years these funds passed through the county. While the county no longer receives these funds directly, they are reported in the county's financial statements as intergovernmental revenues and social services expenditures. In FY2023, this amounted to $324.016 million paid directly to I/DD service providers.

To provide context to some of the financial and economic indicators, we have presented the Great Recession (2008/2009) and the recession that occurred at the onset of the COVID-19 pandemic (2020). Per the National Bureau of Economic Research (NBER): "Contractions (recessions) start at the peak of a business cycle and end at the trough... A recession is a significant decline in economic activity spread across the economy, normally visible in production, employment, and other indicators. A recession begins when the economy reaches a peak of economic activity and ends when the economy reaches its trough...a month is designated as a trough when economic activity reaches a low point and begins to rise again for a sustained period."

- Per the NBER the Great Recession had a peak in December 2007 and a trough in June 2009. "In determining that a trough occurred in June 2009, [NBER] did not conclude that economic conditions since that month have been favorable or that the economy has returned to operating at normal capacity. Rather, [NBER] determined only that the recession ended and a recovery began in that month."

- Per the NBER the recession at the onset of the COVID-19 pandemic had a peak in February 2020 and a trough in April 2020. Similarly, the NBER determined "...hat a trough occurred in April 2020, [NBER] did not conclude that the economy has returned to operating at normal capacity...The [NBER] decided that any future downturn of the economy would be a new recession and not a continuation of the recession associated with the February 2020 peak. The basis for this decision was the length and strength of the recovery to date."

For More Information

The prior reports cover FY1993 through FY2021 and are available on the County Auditor's website. Earlier reports are available upon request.

The county's financial policy is adopted and published annually in its adopted budget. The county's financial statements and budget can be accessed at multco.us.

Additional economic information can be obtained through the State of Oregon for the State Employment Department or the Office of Economic Analysis.

For information about the county's property tax structure and limitations, see the Tax Supervising & Conservation Commission website and the County Assessor's Office website.

For more information about economic recessions, see the National Bureau of Economic Research's website.

Data reliability

For this audit, we used data from Workday, the county's enterprise resource planning system. We assessed the reliability of Workday's data by (1) performing electronic testing for obvious errors in accuracy and completeness, (2) reviewing existing information about the data and the system that produced them, (3) reviewing related documentation, including contractor audit reports, and (4) worked closely with county officials to identify any data problems. We determined that the data were sufficiently reliable for the purposes of this report.

Statement of compliance with government auditing standards

We conducted this performance audit in accordance with generally accepted government auditing standards. Those standards require that we plan and perform the audit to obtain sufficient, appropriate evidence to provide a reasonable basis for our findings and conclusions based on our audit objectives. We believe that the evidence obtained provides a reasonable basis for our findings and conclusions based on our audit objectives.

Audit staff

Michelle Greene, Management Auditor

Annamarie McNiel, CPA, Operations and Audit Director