On this page

- Report highlights

- The county does not report on budgeted versus

- actual expenditures at the program offer level -

- a significant shortcoming of the budget process

- Complexity and short timeline limit potential for public engagement in the budget process

- Recommendations

- Objectives, scope, & methodology

Report highlights

What we found

Multnomah County develops its budget using a complex and time-consuming process, where departments create program offers - individual budgets for programs in their portfolio. The entire budget process takes about eight months. In fiscal year 2022, there were more than 600 program offers ranging from $20,000 to more than $436 million. The county meets Oregon budget law requirements by tracking and reporting on budgeted amounts compared to actual expenditures at the operating fund level by department.

Many components of the county's budget process are consistent with best practices, but the county falls short of best practices in two important areas:

- Financial monitoring - the financial system is not set up to report budgeted compared to actual expenditures on a program offer basis. This means that the county does not publicly report how much it spends at the program offer level - the level at which the Board of County Commissioners makes budget decisions.

- Community engagement - the county has a multi-part approach to community engagement, but the complexity of the budget process and the short timeline available for community involvement limit the potential for impactful public engagement in the budget process.

Why we did this audit

We conducted this audit to assess if the county's budgeting process is transparent and understandable for community members. Like other governments, Multnomah County allocates resources to programs and services that reflect its vision, strategies, and priorities through the budget process. This process is arguably among the most important things governments do.

What we recommend

- The central budget office and Chief Financial Officer should develop an ongoing process for all county departments to report to the Board of County Commissioners at least once each fiscal year to compare the adopted budget to actual expenditures at the program offer level.

- The Board of County Commissioners should develop a policy requiring departments to report to them when they intend to make expenditures in a way that that the Board defines as materially different than how they proposed to spend funds in program offers.

- The Chair should direct the central budget office and departments to engage community budget advisory committees earlier in the budget process so their comments have more time to be addressed before the release of the Chair's proposed budget.

- The Board of County Commissioners should study whether the county should budget on an annual or biennial process and report on the results of this study.

Background

In fiscal year (FY) 2024, Multnomah County's total operating budget was nearly $2.8 billion. The county, like other governments, allocates resources to programs and services that reflect its vision, strategies, and priorities through the budget process. This process is among the most important things governments do.

According to the county's FY 2023 budget director's message,

"the County's budget guides how we make investments in the communities where we live, work, and raise our families. A good budget tells a story about an organization that is not captured by the financial statements. It describes what is important to the organization, how it funds its mission and vision, and how it provides value to the community. These investments reflect the County's shared values and represent the programs and services on which communities depend."

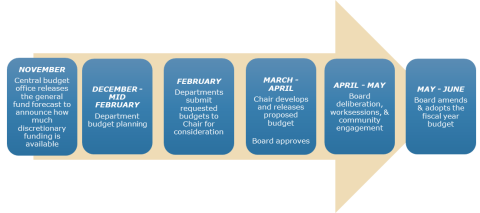

How the Multnomah County budget process works

The budget process takes about eight months and involves staff at all levels of the county. Work on the budget officially begins each November with the central budget office's general fund revenue forecast; the entire process must be concluded by the end of June the following year. At more than $747 million, the general fund is the county's largest source of unrestricted funding and is primarily made up of money collected from property taxes and the business income tax.

The central budget office provides the Board of County Commissioners and departments with financial information and revenue forecasting, as well as program and financial analysis. Based on the County Chair's guidance, the central budget office sets the guidelines for developing, implementing, and adopting the budget. It is responsible for establishing the timeline for completing the budget and for helping departments prepare and administer their budgets.

Departments use information from the Chair and the central budget office to develop a budget request for each program in their portfolio. These individual program budgets are called program offers. Departments create hundreds of program offers in total. The FY 2022 adopted budget included more than 600 program offers ranging from $20,000 to more than $436 million - with a median of about $1.4 million. Some program offers remain largely unchanged from year to year, while others are new requests or are revised from previous years.

Program offers are intended to describe programs and identify how much a department plans to spend on personnel, contracted services, materials and supplies, and other administrative expenses in a way the community can understand. The departments specify where the funding for the programs come from, such as the general fund or a specific state or federal grant. Departments are also supposed to identify and track performance measures for each program budget as well as examine equity issues related to the individual program.

Departments submit their program offer requests to the Chair's Office, and the Chair decides the extent to which their proposed budget will fund the program offers that departments requested. After the Chair releases their proposed budget, the Board holds a series of work sessions, where departments provide an overview of their budget and activities at the department and division level, including some discussion of specific program offers. The Board also holds public hearings where community members are invited to share their views on the proposed budget. Finally, the Board votes to adopt the budget. Then, in four months, departments start the process all over again for the next fiscal year.

Multnomah County budget process timeline

What does a good budget process look like?

Oregon budget law dictates much of how the budget process works. The law specifies the order the process must follow, the minimum requirements for decision making, the minimum standards for public involvement in the process, and a deadline to complete the process.

The Multnomah County Tax Supervising and Conservation Commission (TSCC) is an advisory commission created by the Oregon legislature to oversee budgets, taxes, debt, and management practices of Multnomah County taxing districts. The TSCC holds public budget hearings, conducts annual local budget law training, provides regular advisory services to the county, checks to see that budgets are balanced, and publishes a comprehensive report on local government budgets. The TSCC also plays a role in monitoring the county's compliance with state budget law. Also, the county's contracted external financial auditors evaluate the organization's compliance with state budget law as part of their annual review.

Complying with budget law is a critical part of the process, but the law itself arguably doesn't apply to some of the most important aspects of the process. Because public budgeting is such an important government activity, we wanted to compare the county's budget process to acknowledged best practices for public budgeting. The Government Financial Officers Association (GFOA) has established best practices for the full range of activities involved in developing and adopting a government budget.

Best practices in public budgeting cover a range of issues within each element of the budget process

Development

- Monitored and updated forecast of revenue and expenses

- Structurally balanced budget - Recurring Revenues = Recurring Expenses

- Set priorities and goals

- Public involvement - Start early enough that public input can meaningfully influence decisions

- Develop a budget calendar with specific tasks and a timeline

Justification/Approval

- Decide who to involve, how to select them, and what information will be collected

- Communicate the budget broadly, simply, and clearly

- Empower and foster collaboration among internal departments

- Engage staff at all levels and connect decisions to goals and strategic plans

- Be clear about budget adjustment recommendations

Execution/Accountability

- Monitor and evaluate stakeholder satisfaction with programs and services

- Review relationships between economic indicators and potential impacts

- Reporting - Monitoring results should be communicated

- Expense and revenue monitoring - Budgeted versus Actual

- Performance Measures - Identify variance between budgeted and actual performance

Source: Auditor's Office, based on a review of GFOA public budgeting best practice literature

Note: According to the GFOA, a structurally balanced budget matches revenue that can predictably be expected to continue from year to year, like property tax revenue (recurring revenue), with expenses that show up in the budget every year, such as program personnel costs and contracts (recurring expenses). In a structurally balanced budget, unexpected revenue should only be spent on projects that do not require ongoing expenditures, such as a one-time-only grant, or should be added to reserves.

Developing Multnomah County's budget is extremely complex and time intensive, given the county's diverse lines of business - from health clinics to library branches to law enforcement - and the billions of dollars involved. During the course of the audit, we noted the considerable knowledge and expertise of county staff in the central budget office and departments.

The county does not report on budgeted versus

actual expenditures at the program offer level -

a significant shortcoming of the budget process

The Government Financial Officers Association's (GFOA) financial monitoring best practices stress the importance of monitoring and reporting on what is budgeted compared to actual expenditures to enforce accountability and demonstrate transparency. The county budgets at the program offer level, but does not report on actual spending based on program offers. This makes it difficult, if not impossible, to meet best practices for financial monitoring.

Budgeting best practices stress the importance of monitoring and reporting budgeted compared to actual expenditures

The GFOA recommends that all governments compare budgeted to actual results to monitor financial performance. Similarly, Oregon law requires that governments within the state report budgeted compared to actual expenditures and to show that the government has not overspent its budget.

The county meets Oregon budget law requirements by tracking and reporting on budgeted amounts compared to actual expenditures at the operating fund level by department. This is a high level that is based largely on the source of revenue for the fund and the type of restrictions on its uses, such as the general fund (for unrestricted revenue) and the state and federal fund (for state and federal grants that are restricted to use for specific purposes). However, county departments present their budgets to the public and the Board at lower levels, including the program offer level.

According to the GFOA, a government should be able to show if it has actually purchased goods and has actually provided services. Proper monitoring of budgeted compared to actual expenditures also includes analysis by category, for example:

- Personnel. Did the organization hire the staff it was budgeted to hire and were these costs consistent with expectations?

- Contracted Services. Are services being provided as anticipated? Are any services being provided that were unanticipated? What trends are being observed that may impact whether or not spending remains on track?

While the GFOA doesn't specify the level at which this analysis should be performed, we believe that to support transparency it should be done at the program offer level - not just at the operating fund level. The program offer is the foundational unit of the county's budget and represents a pledge to county residents to devote resources to specific services. It is the level at which the Board makes budget decisions.

The county's financial system is not built to report budgeted versus actual on a program offer basis

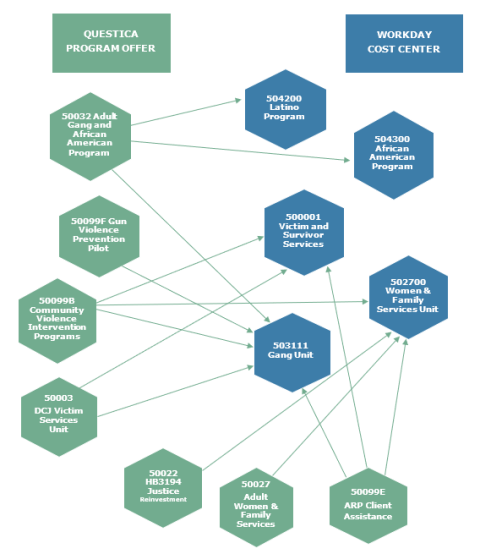

The county develops its budgets using a system called Questica, and the budgets are built on the basis of individual programs (or groups of similar programs) that are called program offers. The county's system of record for finance is an enterprise resource planning system called Workday. This system is where the county tracks revenue and spending and is the source of financial reports.

Workday is organized differently than Questica in two important ways. First, Workday uses organizational units called cost centers that individual departments create based on the way they operate. Cost centers do not necessarily line up with Questica's program offers. For example, there may be multiple cost centers assigned to a single program offer. Departments do this, at least in part, so they can best account for the way different parts of their operations are funded and the different agreements that come with that funding.

In some cases, the program offer and cost center do line up. And, in these cases, it is possible to report budgeted compared to actual expenditures from Workday. However, there are still 135 cost centers that do not line up, making routine reporting very difficult.

This example from the Department of Community Justice illustrates the common issue of how more than 100 cost centers and program offers don't line up

The above visualization reflects just one instance where the program offers created in Questica did not match the Workday cost centers. This next example illustrates a similar situation, but with actual budget numbers.

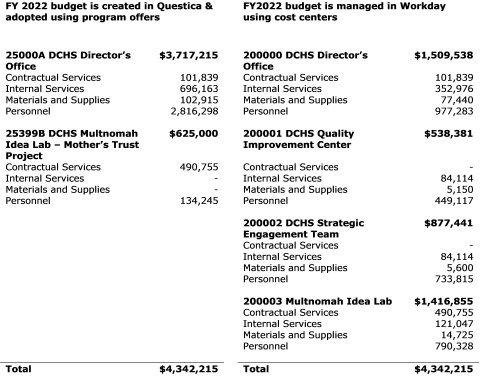

The Department of County Human Services Director's Office program offer includes three complete cost centers' budgeted funding: the Director's Office, the Quality Improvement Center, and the Strategic Engagement Team. It also includes part of the Multnomah Idea Lab.

To report actual expenditures for the Director's Office program offer, you need to add the expenditures for all four cost centers and then subtract the portion of the Multnomah Idea Lab's expenditures that belong to the Mother's Trust Project program because that has its own separate program offer. The Mother's Trust Project does not have its own cost center, and is part of the Multnomah Idea Lab cost center.

A detailed comparison of adopted program offers and cost center budgeted expenditures for the Department of County Human Services Director's Office

Being able to accurately monitor and report budgeted compared to actual expenditures is also important for the county to know if it is spending according to the adopted budget and if that spending is helping the county achieve its objectives. Management should report this information both internally and externally to the community, but it does not.

Management can report internally on actual expenditures on a cost center basis, as well as at the division and department levels. For example, the Department of Community Justice uses data dashboards that identify budget compared to actual expenditures at the department, division, and cost center levels. In addition, they show this comparison for major spending categories, such as personnel, materials and services, contracted services, and capital. The department uses this information for internal management and shares it with its community budget advisory committee.

We combined data from Questica and Workday in an attempt to match cost centers to program offers. Then we compared budgeted to actual expenditures by program offer. Where we could line up cost centers with program offers, we found some significant variations. For example, in the Health Department, nearly 20% of large program offers that lined up with cost centers were over or under budget by at least 15%. The department as a whole was under budget by almost 15%.

Some variations between budgeted and actual expenditures are to be expected. For example, a program that has budget authority to hire additional staff would have to hire all that new staff immediately at the start of the new fiscal year at the budgeted salary in order to use all of the budgeted amount for personnel. New staff are very rarely hired that quickly, meaning that the program would underspend its personnel budget. Similar situations occur with contracted services spending. It is not uncommon for a program to underspend its contracted services budget if the revenue (such as state or federal grants) for the budgeted service doesn't get to the program until sometime in the middle of the year. Or, a department may receive a grant at a different amount than expected in the budgeting phase that took place months earlier.

Departments report how much they under or overspend on personnel and other budget categories to the central budget office and typically to their community budget advisory committees, but are not required to report the specifics of these deviations. However, when a department needs to make a significant change to its budget, there is a formal process for modifying the budget. Circumstances requiring a formal budget modification include:

- Increases or decreases in revenue or appropriations,

- Increases or decreases in full-time equivalent staffing,

- Transfers between major funds,

- Transfers from fund contingency,

- Position reclassifications, and

- Significant policy or programmatic changes, even if the impact nets to $0.

Department managers told us they consult with the central budget office about significant deviations from budgeted expenditures, but the central budget office has no way to monitor this activity using the existing systems.

The county should monitor and report on budgeted compared to actual expenditures at the program offer level

County management agreed that being able to monitor and report on budgeted compared to actual expenditures at the program offer level is an important piece of a high-functioning budget process. They said that county staff had been working on addressing this issue until the pandemic interrupted their efforts. The FY 2024 budget includes a note specifically addressing new financial reporting efforts, directing the Chief Operating Officer to work with departments and the Chief Financial Officer to "explore options to coordinate and develop countywide budget to actuals reports." However, the note does not specify that these budget to actual reports be completed at the program offer level, which we recommend.

Moving to a two-year budget cycle would also help improve transparency in budgetary spending. As the process currently stands, a fiscal year is only about half completed by the time the departments prepare program offers for the next fiscal year. Stretching the process out to two years would allow the county to report on budgeted compared to actual expenditures from the first half of the budget biennium in the program offer for the following year.

Complexity and short timeline limit potential for public engagement in the budget process

The county's approach to public engagement addresses many of the Government Financial Officers Association's (GFOA) best practices. The county uses a multi-pronged approach to obtain community feedback on priorities: including community budget advisory committees (CBACs); public hearings on the proposed budget; direct outreach to community groups by the Chair's Office; and departmental outreach through advisory groups and discussions with community partners. A combination of factors, including the complexity of the process itself, the compressed budget development and approval schedule, and a general lack of understanding about county functions among community groups work against effective community engagement in the process.

County's multi-pronged approach meets many best practice criteria

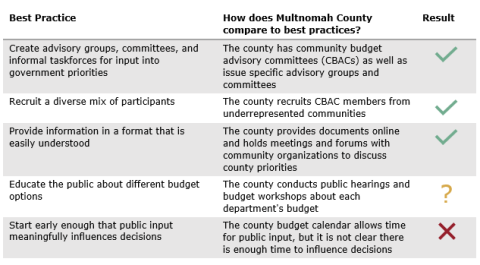

According to the GFOA, effective public engagement practices can foster a government's responsiveness and accountability to their communities. To ensure an effective, well-implemented public engagement, the GFOA recommends a variety of approaches, including:

The county has a multi-pronged, diversified approach to educate community members and solicit their input on county priorities. Taken together, this approach meets many of the GFOA's best practices.

Best practice: Create advisory groups, committees, and informal taskforces

County's practice: The county operates community budget advisory committees (CBACs) - one for each department, one for the Library, one each for the Sheriff's and District Attorney's Offices, one for the remaining elected officials and small offices, and a countywide central CBAC. According to the County Code, CBACs were created to foster community involvement in the budget process and as an improvement over previous budgets in informing communities about county budget problems, processes, and proposals.

CBACs are one of the key ways that the county receives community input on its budget priorities. CBAC volunteers hear directly from leadership and other staff about the county's programs and services. Together, they make recommendations to the Board of County Commissioners about how Multnomah County can best use its resources to serve the community. In addition to CBACs, there are more than 20 advisory committees made up of community members that advise departments and elected officials on a range of specific topics, from food services to behavioral health issues.

Best practice: Recruit a diverse mix of participants

County practice: The Chair's Office works with the county's Office of Community Involvement to recruit diverse membership for CBACs. In addition, Chair's Office policy advisors have been responsible for identifying community organizations to reach out to regarding priorities and the budget. The Chair's Office coordinates these activities that involve education about the budget process as well as about how county efforts have been performing. Chair's Office staff told us that their outreach efforts tend to concentrate on communities who are underrepresented in access to county leadership.

Best practice: Provide information to the public in a format they can understand

County practice: According to the central budget office, the primary goal of a program offer is to help make the budget understandable to communities within the county. The county provides budget documents online, holds workshops and hearings to provide information, and meets with community groups. When the Chair's Office policy advisors meet with community groups, they usually include the appropriate department staff. This way, the community groups can have questions answered, make requests, and provide feedback on how programs are performing.

Best practice: Educate the public about different budget options

County practice: Oregon budget law requires local governments to hold at least one public hearing on the budget and to provide the public with the opportunity to comment on the budget. Multnomah County holds several public hearings on the budget. The county also has public work sessions with presentations from individual departments prior to the vote to adopt the budget. The public is invited to attend and may give testimony at the public hearings.

Department directors told us that department work with community members is focused on their CBACs, individual issue-specific advisory committees, and contracted community partners. However, most of the interaction with advisory committees and contracted community partners is not about general county budget priorities, but rather about department-specific issues.

Best practice: Start the budget process early enough that public input meaningfully impacts decisions

County practice: It is not clear how much impact community engagement efforts have on budget priorities. CBACs have a specific mandate to provide input on departmental budgets, and some meet year-round to gather and respond to information the department provides. Public hearings give the general public the opportunity to comment on the proposed budget prior to its adoption. These tend to take place in May, the month before the Board adopts the budget. Much of the community engagement specific to the budget occurs either right before or after the release of the Chair's proposed budget. The amount of work that goes into the Chair's proposed budget, combined with the short time to required adoption, creates a disincentive for the community engagement to have a substantial impact on budget priorities.

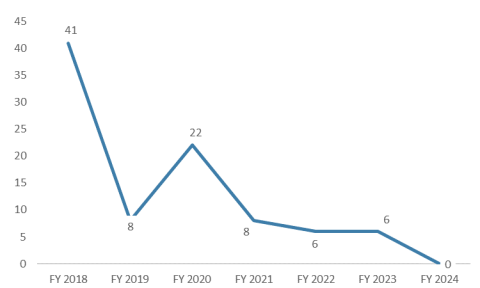

One of the primary jobs of a CBAC is to provide a letter to the Chair that outlines the committees' issues regarding the department budget they are charged with reviewing, but CBACs rarely get those letters to the Chair in time to have an impact on the budget. In three of the last four years, CBACs submitted budget letters fewer than 10 days before release of the Chair's proposed budget. With this in mind, it is not surprising that CBAC members surveyed by the Office of Community Involvement said they did not believe their input had an impact on the budget.

CBACs submit budget recommendation letters late in the process

Median number of days between CBAC letters submitted to release of the Chair's proposed budget

The Chair's proposed budget represents the total amount available to spend on county programs and services. County budget hearings about this proposed budget are arguably the most visible component of the budget process. The public budget meetings are extensive, involving all departments. County management told us that Commissioners' amendments to the proposed budget may reflect community testimony at the public hearings or community outreach to individual Commissioners. Overall, the May budget hearings do not appear to have much impact on the Chair's proposed budget. There is little additional funding available, and any significant change to the budget would be very difficult at this stage in the process because it could potentially mean having to modify multiple program offers before budget adoption in June.

Community groups we contacted had mixed experiences with communicating priorities to county policy makers. While our sample was limited, it appeared that community organizations with financial partnerships with the county better understood the process. Communication between departments and community organizations is more focused - around specific programs - and usually only involves organizations that have contracts with the departments.

Community engagement efforts would benefit from the added time that comes with a two-year budget cycle

There are positives and negatives associated with the county's program offer approach to developing its budget. On the positive side, program offers provide information about what the county intends to do. On the negative side, budgeting using program offers uses a tremendous amount of county resources and takes a great deal of time. Effectively engaging community is also time intensive.

Moving to a two-year budget cycle would help alleviate some of the challenges facing community engagement efforts in the budget process we identified, specifically educating the public about different budget options and starting early enough that public input can meaningfully influence decisions. Short of moving to a two-year budget cycle, the county should look to consolidate program offers to reduce workload in developing the budget. Consolidating program offers would likely shorten the time needed to create program offers because there would be fewer program offers to create, which could mean there would be more time for community engagement. And, the county should encourage departments to engage CBACs earlier in the process and provide them with information sooner, so their comments have more time to be addressed with the release of the Chair's budget.

Recommendations

- To improve transparency, the central budget office and Chief Financial Officer should develop an administrative procedure requiring all county departments to report to the Board of County Commissioners at least once each fiscal year on revised budget to actual expenditures at the foundational unit of the county's budget, which is currently the program offer level. Due date: September 30, 2024

- To improve transparency, the Board of County Commissioners should develop a policy requiring departments to report to them when they intend to make expenditures in a way that the Board defines as materially different than how they proposed to spend funds in program offers. Due date: September 30, 2024

- The Chair should direct the central budget office and departments to engage community budget advisory committees earlier in the budget process and provide them with information sooner, so their comments have more time to be addressed with the release of the Chair's proposed budget. Due date: September 30, 2024

- The Board of County Commissioners should study whether the county should budget on an annual or biennial process and report on the results of this study. Areas to study could include potential impacts on community involvement in the budget process, budget inputs and outcomes, and monitoring of adopted budget to actual expenditures. Due date: September 30, 2024

Objectives, scope, & methodology

The objectives we focused this audit on were:

- Does the Multnomah County budget process meet best practices with regards to community involvement?

- Is the county providing the appropriate information to the public in terms of its financial monitoring of budgeted vs. actual expenditures?

To accomplish these objectives, we reviewed the literature on best practices in public budgeting, Oregon public budget law, county budget policies, county budget preparation documents, and the budgets themselves for the last four fiscal years. We concentrated on best practices developed and published by the Government Financial Officers Association (GFOA). We limited our review to two aspects of GFOA best practices in public budgeting: 1) Monitoring of budgeted versus actual expenditures and 2) the extent to which the county uses public engagement to help establish its priorities for budgeting.

With financial monitoring, we reviewed budgeted and actual expenditures for FY 2022, using both the Questica and Workday data systems. And we looked at community budget advisory committee (CBAC) activities for fiscal years 2018 through 2024, as well as the Chair's proposed general fund budget compared to the adopted budget for those same fiscal years. In addition:

- We talked with each department about monitoring and reporting efforts and potential shortcomings.

- We compared budgeted vs actual spending starting at the department level for general fund as well as state and federal grant funds and down to the cost center level to illustrate where differences between the two begin to present themselves.

- We interviewed central budget office staff about financial monitoring practices.

- We reviewed summary level budget data from FY 2023 and 2024.

- We interviewed department directors to obtain information about how they use community engagement to establish departmental priorities.

- Combined the results of CBAC surveys administered by the Office of Community Involvement, email questionnaires, and interviews to determine how well community groups and CBACs understand the process and perceive that they have an impact.

- Interviewed the prior Chair's Chief of Staff, each department director (and some division directors), the budget director, the chief economist, the TSCC staff and one TSCC member, and a number of community partners.

We conducted this performance audit in accordance with generally accepted government auditing standards. Those standards require that we plan and perform the audit to obtain sufficient, appropriate evidence to provide a reasonable basis for our findings and conclusions based on our audit objective. We believe that the evidence obtained provides a reasonable basis for our findings and conclusions based on our audit objectives.

For this audit, we analyzed budget and financial data for the time period of July 1, 2021 to June 30, 2022 (fiscal year 2022) from Workday, the County's enterprise resource planning system. We assessed the reliability of Workday's data by (1) performing electronic testing for obvious errors in accuracy and completeness, (2) reviewing existing information about the data and the system that produced them, (3) reviewing related documentation, including contractor audit reports, and (4) worked closely with county officials to identify any data problems. We determined that the data were sufficiently reliable for the purposes of this report.

We assessed the reliability of Questica, the County's budget software, data by (1) performing electronic testing for obvious errors in accuracy and completeness, (2) reviewing related documentation, and (3) interviewing county staff knowledgeable about the data. We determined that the data were sufficiently reliable for the purposes of this report.

Audit staff

Mark Ulanowicz, CIA, Principal Auditor

Sura Sumareh, Management Auditor