Pandemic Funds: Management has policies and procedures in place to manage pandemic funds

Pandemic-Related Funding and Expense

Objective, Scope, & Methodology

What We Found

In this audit, we found that county management sought to balance the need to get resources out to the community quickly with also maintaining effective policies and procedures to help manage the county’s spending of pandemic-related relief funds. We found several areas where the county managed policies and procedures well; we also found some areas for improvement:

- The county appeared to spend in alignment with its stated commitment to leading with race, based on funds expended with the intent to serve culturally specific community members, including Black, Indigenous, and People of Color community members, as well as partnering with new providers that had connections to culturally specific community members.

- Management ensured policies and procedures were in place to manage pandemic spending. For example, the county provided guidance to code and track pandemic-related expenses that would be eligible for payment with federal pandemic funding such as from the CARES Act, helping to ensure that the county did not leave federal pandemic funds unspent.

- Under the County Chair’s emergency declaration, the county’s purchasing division approved a limited number of waivers to allow for contracting without a competitive bidding process. This provided flexibility to county departments to meet the emerging and urgent needs of the county and communities they serve.

- As the pandemic negatively affected some community members financially, the county developed processes and procedures to provide direct financial assistance to community members.

- We found a work unit circumvented procedures in the use of a county procurement card (p-card, similar to a credit card) in one instance. This resulted in the county paying a vendor that had been convicted for theft and false claims for medical billing. The county initially made these payments from federal pandemic-related grants (mostly the CARES Act), which was not allowed since the vendor was on the federal government’s list of excluded vendors.

- We identified a transaction in which the county paid the wrong vendor, resulting in an overpayment to one provider organization and a non-payment to another.

- Provider organizations reported that they generally had positive experiences working with the county to distribute pandemic funding, but they also reported barriers to eligibility for some community members and not enough funding to go around.

Why We Did This Audit

The COVID-19 pandemic has presented significant challenges to Multnomah County. We conducted this audit to support transparent and accountable government operations during this unprecedented time. This report details what the county spent pandemic funding on, which provider organizations received pandemic funding from the county, and whether funds were distributed in alignment with the county’s stated commitment to leading with race. It also details our work and findings regarding policies and procedures related to procurement, contracting, contract management, inventory management, and fraud risk, and information gleaned from provider organizations through our survey about working with the county to provide pandemic-related relief funding and services to community members.

What We Recommend

- We recommend that Central Accounts Payable provide enhanced procurement card (p-card) training to all county staff that use and/or manage p-card transactions by December 31, 2021. We recommend this enhanced training highlight that services cannot be paid for by p-card, p-cards are not to be used to circumvent accounts payable controls, the responsibility of the review and approval roles, and emphasize the consequences of not following county policies, which include but are not limited to p-card privileges being revoked.

- We recommend the Chief Financial Officer’s office develop a centralized detective control for identifying improper use of p-card transactions. A detective control is a procedure to identify errors or problems after they have occurred. This process should be in addition to Central Accounts Payable periodic audits and include a comparison of p-card vendors to the federal Systems for Award Management (SAM.gov) list. We recommend this process be performed at least quarterly and be put in place by December 31, 2021.

- From the issuance of this report through at least the end of 2022, the County Chair and Government Relations should continue to communicate frequently with Oregon's state legislature and federal delegation about rent assistance requirements that were barriers to helping people in need, particularly Black, Indigenous, and People of Color community members, receive assistance during the COVID-19 pandemic.

- We recommend that by December 31, 2021 the Health Department evaluate the employees assigned to approval roles to ensure their workload capacity is appropriate to effectively and adequately review transactions before completing an approval step in Workday.

- We recommend that by December 31, 2021 the Health Department enhance their detective controls to ensure that routine reconciliations of vendor payments are performed, to help identify any mispayments, such as monthly contract reconciliations of vendor invoices for what has been paid compared to what has been invoiced, to date.

Pandemic-Related Funding & Expenses

Our audit objectives included determining what pandemic-related funds the county received or was eligible to receive in fiscal year 2021 (FY2021) and where the county spent FY2021 pandemic-related funds, as well as determining if the county made efforts to distribute FY2021 pandemic funds in alignment with the county’s stated commitment to leading with race. The following provides summaries of the pandemic-related funding received and spent in FY2021. FY2021 was the period of July 1, 2020 through June 30, 2021.

Total Pandemic-Related Funding Recognized in Fiscal Year 2021 was $159.5 million

The data presented in the charts below represents pandemic-related funding recognized by Multnomah County for FY2021. It does not include any county general funds that were used to support pandemic-related costs/efforts. Additionally, it does not include revenues related to ongoing funding sources. We coded revenues based on a review of the coding in the county's financial software and through a review of county budget documentation.

- Funding Received Summary

- Pandemic-Related Funding Recognized by County Department in Fiscal Year 2021 (over $100,000)

- Other Funding Received by Department

Total Pandemic-Related Expenditures in Fiscal Year 2021 was $159.3 million

The data presented in the charts below represents expenditures coded to pandemic-related funding sources. It does not include any county general funds used to support pandemic-related costs/efforts. Additionally, it does not include expenditures related to ongoing funding sources.

We categorized expenditures with the objective of helping the public understand the county’s generalized pandemic-related expenditures in FY2021. We based the categories on a review of the coding in the county's financial software and through a high-level review of supplier invoices and contracts.'

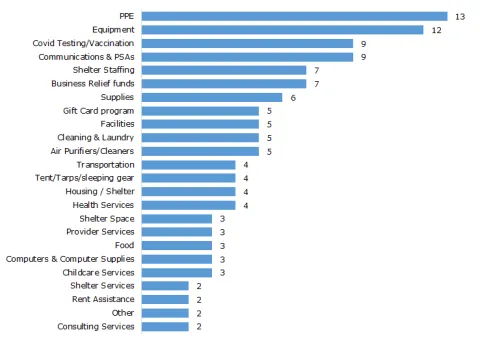

Pandemic-Related Expenditures by Program/Service

Expenditures are summarized into the following categories:

- Rent/Mortgage/Motel/Utilities Assistance – this is the direct payment of a community member’s rent, mortgage, motel stay (includes payments to property owners/managers for space leased for voluntary isolation motels/space), garbage, electric, phone, and/or internet bill. These payments were made either directly by the county or through a partner organization such as Home Forward.

- Personnel Costs –includes the direct county labor costs as well as the county’s costs for temporary staffing agencies.

- Provider Services – includes shelter and emergency housing services, culturally specific health workers and mental health services, and other client assistance

- Land/Building/Structure Purchases/Repairs - includes land & building purchase of the property at 1952 N. Lombard & the old Days Inn on NE 82nd, pallet shelters (temporary mobile tiny homes), and shelter/motel modifications/repairs.

- Business Relief Funds program – financial operational support to food establishments impacted by COVID-19. This funding was provided directly to over 2,780 businesses through the county. Additionally, businesses in Multnomah County received funding through partner organizations including Portland Business Alliance Charitable Institute, the Black American Chamber of Commerce, the Philippine American Chamber of Commerce, Asian Pacific American Network of Oregon, and the Native American Youth and Family Center.

- Food – includes the Food Justice program, shelter and community direct food preparation and delivery, provided by culturally specific partner organizations, and other direct food purchases.

- Gift Card Programs – includes the large infusion of cash-equivalence intended to provide flexible client assistance quickly and to make funds available to community members to obtain necessary items.

- Infection Control Supplies– includes Personal Protective Equipment (PPE), masks, gowns, gloves, and sanitizing supplies.

- County Internal Services – personnel and supplies costs for internal support services for facilities requests (shelter janitorial and security services), installing Plexiglas, and various other property management and IT support costs

- Supplies – various supplies to support the pandemic‐related emergency in all departments including medical supplies for Health Department clinics, computers & computer supplies to assist in getting county personnel moved to a remote working environment, and clothing/linens/hygiene supplies for shelters.

- Tents/Tarps/Sleeping gear – provided directly to community members in need.

- Facilities & Administration (F&A) – amount expensed for support costs (e.g. administering the pandemic-related funds) which, while not allowed by the Coronavirus Relief Fund (CRF), was allowed under some of the other grant funding.

- Lab Testing & Vaccination Services – including COVID-19 vaccines.

- Other – see the tab detailing out other expenditures below.

- Cleaning & Laundry Services – includes laundry, cleaning, and pest control services at motel and shelters sites.

- Equipment – includes a mobile COVID-19 testing van, sterilizer equipment, radios for the Sheriff’s Office to assist with social distancing, and Elections equipment.

- Communications & Public Service Announcements (PSAs) – includes third-party call centers services and purchased time for announcements made on radio and television.

- Vaccine & Testing Space – costs associated with the space for COVID-19 community testing and vaccination sites.

Expenditures Categorized as Other was approximately $670,000

Below is a graph of the pandemic-related expenditures categorized as “Other” in the graph above. The remaining $111,000 within the “other” category in this grouping represents costs across various departments and includes purchases for health clinics as well as expenditures for various direct client assistance.

Pandemic-Related Expenditures Categorized as "Other" in the graph above

Total Pandemic-Related Personnel Expenditures for FY2021 was $34.38 million

Pandemic-Related Personnel Costs by County Department in FY2021 Data below presented in millions

Pandemic-Related Expenditures by Provider/Supplier

Pandemic-Related Expenditures by Providers/Suppliers (over $100,000)by County Department for FY2021

The County Provided $58.7 Million for Pandemic-Related Expenditures to Over 70 Service Providers in FY2021. The Majority of these Providers Provided Some Level of Culturally Specific Services with Pandemic-Related Funding

One of our audit objectives was to see whether the county made efforts to spend pandemic-related funds in alignment with its stated commitment to lead with race. We found that the county appeared to spend in alignment with this commitment, based on funds expended with the intent to provide culturally specific services, including services to Black, Indigenous, and People of Color community members, as well as partnering with new providers that had connections to provide culturally specific services.

Below are graphs showing providers (other than Home Forward) that received $25,000 or more from the county for pandemic-related expenditures in FY2021 to assist with programs such as:

- Housing and Rental assistance programs (does not include direct payments to landlords/property managers/financial institutions for motel rooms/rent/mortgage payments or direct payments to utilities/phone/internet companies/contractors)

- Business Relief Fund program

- Food programs – such as the Food Justice program, meals provided by culturally specific partner organizations, and shelter and community direct food preparation and delivery (does not include direct purchase of food/water supplies from retailers)

- Other Provider Services – such as shelter and emergency housing services, culturally specific health workers and mental health services, and other client assistance

Note: Home Forward accounts for approximately $27.5 million in pandemic-related expenditures. The graphs below do not include Home Forward because visualizing the funding that went to Home Forward overshadows the rest of the visualization. Nearly all (over 99%) of the expenditures associated with Home Forward were for rental assistance programs. The county’s contracts with Home Forward include culturally responsive strategies and/or priorities.

The County Worked With Over 70 Service Providers to Extend Programs/Services to Community Members in Four Major Categories of Program/Services Expenditures in FY2021

Sixty-one (80%) of the 76 providers in this analysis were noted as a culturally specific organization, or some or all of the expenditures for the provider were intended to provide culturally specific services. Ten providers (13%) had culturally specific strategies/priorities included in their contract with the county. The remaining five (7%) had contracts for providing more generalized services (e.g. meals to shelters, services for incarcerated individuals).

The County Leveraged Several New Providers to Assist in Getting Support to the Community Since the Pandemic Started

Twenty-two (29%) of the 76 providers, for $5.9 million in expenditures, had not provided services on behalf of the county prior to the county emergency declaration for the COVID-19 pandemic (March 2020). The county appeared to make an effort, with programs such as the Food Justice and Business Relief programs, to leverage these new providers because of their connections to provide culturally specific services.

County management allowed for some policy and procedure exceptions in order to respond to urgent needs brought on by the pandemic for supplies and client assistance

Management ensured policies and procedures were in place to manage pandemic spending in the county’s financial and human resource system of record, Workday (enterprise resource planning (ERP) system). This included guidance to code and track pandemic-related expenses that would be eligible for payment with federal pandemic-related funding such as via the CARES Act.

The county maintained most of its standard procedures to manage pandemic spending and made some changes to expedite the process

The pandemic presented the county with new, unforeseen expenses, such as for protective equipment supplies like gloves and masks, additional public health resources, shelter and quarantine space, and direct financial assistance to community members. Early in the pandemic, the county’s Chief Financial Officer worked with finance units throughout the county to ensure that pandemic-related costs were specifically coded as pandemic related in the county’s financial and human resource system of record, Workday. In the original CARES Act, there was a spending deadline of December 30, 2020. This deadline presented some risk: if the county did not spend all of the CARES Act funding it received by the deadline, or if in the rush to get money out the door the county spent CARES funding on ineligible expenses, it may have to return funds to the federal government.

The county had policies and procedures in place prior to the pandemic, and for the most part the county continued to use those processes throughout the pandemic. However, in the interest of purchasing pandemic-related supplies as needed, quickly, and in the interest of reaching community members with direct assistance, the county’s declaration of emergency suspended purchasing rules. This allowed for changes to processes and for some exceptions to standards. For instance, the county:

- provided advance payments to some provider organizations;

- waived the requirement to use a competitive process for purchases;

- distributed $5 million in gift cards, in individual amounts as high as $599, as a means of direct assistance to community members.

We heard from management about balancing the need to distribute funds quickly with also being conscious of maintaining effective policies and procedures to help ensure compliance with the county’s spending of pandemic funds. In some areas, the county was willing to accept more risk to meet community need.

The county made exceptions to contracting rules to manage supply and service needs

The pandemic presented another challenge with regard to goods and services: Some supplies and services were in short supply, and the county had to pivot to new suppliers in some situations. The Chair issued an emergency proclamation on March 11, 2020, which among other things, suspended Public Contracting Review Board (PCRB) requirements for buying pandemic-related goods and services, such as food, shelter, laundry services, masks and gloves. Elements of the PCRB rules include that the county will allow impartial and open competition in its contracting. This helps ensure the county does not overpay for goods and services, while also ensuring opportunity for many suppliers and contractors to earn the county’s business. Under this emergency declaration, the county purchasing manager had the authority to issue waivers, if needed, from the PCRB requirements.

Reflecting the circumstances brought on by the pandemic, and the need to buy from new suppliers relatively quickly, the county purchasing manager approved a total of 122 waivers for 116 suppliers between March 11, 2020 and August 31, 2021, for goods or services directly related to the pandemic. These waivers provided the needed flexibility to county departments to move more quickly in meeting urgent community needs.

The county granted waivers from standard purchasing requirements across broad categories of pandemic-related goods and services, but most commonly for personal protective equipment (PPE)

While these waivers did allow for sole source contracting without a competitive bidding process, the purchasing manager told us they worked with senior leadership and encouraged county departments to utilize existing processes whenever possible, such as seeking multiple bids, to promote a competitive procurement environment.

Health Department suppliers received the greatest number of waivers from standard purchasing requirements

The Board of County Commissioners extended the emergency declaration to December 31, 2021, which allows for a continued waiver from the PCRB requirements. After December 31, 2021, the waivers allowed under the emergency declaration will no longer be an available option for departments, unless the Board extends the emergency declaration.

The county is still using waivers, but since the peak in November of 2020 - as the initial CARES Act expiration date approached - the number of requests for waivers diminished

Between March 11, 2020 and August 31, 2021, the purchasing manager granted a total of 122 waivers to 116 suppliers, yet the county initiated a contract or purchase for goods or services for 839 suppliers during that time period. While it appears that the county purchasing manager has handled waivers to the PCRB rules responsibly, granting waivers for only a fraction of the contracts approved since the pandemic began, departments should wind down the use of waivers as the pandemic recedes to help increase competitive opportunities for business with the county. The county’s purchasing manager indicated they are working with departments to get plans in place to move away from exemptions and be prepared to go back to the PCRB competitive processes by December 31, 2021.

Direct financial assistance supported urgent community needs

As the pandemic negatively affected many community members financially, the county sought additional ways to provide direct financial assistance to community members.

A primary program of direct financial assistance using pandemic funds was the Food Justice program, which the Department of County Human Services (DCHS) developed with County Treasury. DCHS’ intention for this program was to provide direct financial assistance to community members in Multnomah County affected by the pandemic. This program distributed about $2.9 million to community members partially in the form of gift cards. The program had these primary objectives:

- To provide pandemic-related relief to community members, particularly Black, Indigenous, and People of Color in east county affected by the pandemic. Distribute the relief by December 30, 2020, the original CARES Act deadline.

- Issue the payments in a secure way, using protocols that would reduce the risk of fraud or loss.

Tangentially, the Health Department distributed gift cards to clients of the Special Supplemental Nutrition Program for Women, Infants and Children (WIC) and Early Childhood Services programs. The Health Department distributed about 8,000 gift cards in $500 denominations, for a total of about $4 million.

Gift cards are inherently risky because they are similar to cash; it is difficult to ensure that they are used only by the intended recipient, and for the purpose intended. This makes it important to ensure segregation of duties in purchase, receipt, storage, and distribution. The county has rules regarding the use of gift cards, which include:

- Cash Equivalents should only be used for client incentives, client assistance, or volunteer payments for one-time only events.

- Individual Cash Equivalents (per item) must be valued at $50.00 or less.

- Cash Equivalents must be treated as cash and kept in a secure and locked location only accessible to authorized county staff.

- Cash Equivalent disbursements must be properly tracked and documented to ensure proper usage. Each purchase order must have a separate tracking log

County management stated that given the urgency of the need for direct assistance, and the initial deadline to spend CARES Act funds by December 30, 2020, it was worthwhile to accept some risk and loosen the gift card usage rules in developing a gift card distribution program rapidly. County Treasury worked closely with DCHS and the Health Department to ensure the gift card distribution would be secure, and Treasury helped track payments that the county mailed out directly.

There were three primary distribution methods for gift cards to provide pandemic-related relief to community members:

- Gift cards were sent directly from the program, working closely with Treasury, and Treasury had the ability to track those cards for use and delivery.

- Gift cards were distributed by program staff to clients/community members, at organized events, typically hosted by provider organizations.

- Provider organizations working under contract with the county purchased gift cards on their own, distributed those gift cards directly to community members, and billed the county through a cost reimbursement contract.

As far as the first two methods, the county has records to indicate to whom the gift cards were distributed. There were few reported instances of card loss or theft. Regarding the third method, the county requested that provider organizations track the delivery of cards to community members, but they were not required to submit documentation to the county unless requested.

We found the county had adequate documentation of gift card distributions for the first two methods. The county did not collect detailed documentation for the last method. For cards purchased and distributed by provider organizations, the county is not monitoring the control and distribution of the cards. Some of these cards could be subject to loss, unintended destruction, or theft. County management said that they felt this risk was minimal compared to the use. The use in this case was to make a large infusion of cash-equivalence available to the community to provide flexible client assistance quickly and to make funds available to community members to obtain necessary items.

Controls for county procurement cards were circumvented in one instance

Due to the volume of financial resources received from the federal government, state, and other local agencies (for example, CARES Act funds), and the speed at which the funding needed to be spent (by December 30, 2020 until a last minute extension in late December 2020) we believed there to be an increased risk that the funds may be used inappropriately.

To partially address this risk, we reviewed pandemic-related purchases made with county procurement cards (p-cards), similar to a credit card. P-cards have long established protocols for payments and approval.

The county hires contractors and provider organizations to provide services in a variety of areas such as counseling, health services, and translation. County policy requires that payment for these services go through the county’s payment processing system, which is Workday. Assuming the correct approvals, purchases of goods such as supplies and materials can be made with p-cards. We identified a vendor that the county paid for services by p-card, which is against county policy. The county employee who initiated the payment should not have paid for these services with a p-card, and as part of the approval process, county management should have identified this violation of p-card procedures.

Upon additional review of the payments to this vendor, we found that the vendor had been inactivated in Workday, with a notation that the vendor was under investigation by the Oregon Department of Justice. The inactive status in Workday should have worked as an effective control, preventing the county from paying the vendor directly through Workday. A county employee circumvented this control by paying the vendor by p-card.

We notified county management of the situation, who initiated a review of the payments. Initially, management decided to continue payments to the contractor, and instead process the payments using Workday. In our further review of the situation, we found that the vendor had been convicted in 2020 of multiple counts of felony theft and false claims for medical billing, and we notified management of this fact. Management ultimately halted services from and payments to the vendor.

Several control failures occurred in this instance. When the supplier submitted the invoice for services rendered, the county employee responsible should have initiated the payment in Workday. Instead, the employee responsible initiated the payment by p-card. The responsible employee’s supervisor then approved the payment, and submitted the approval to the person designated to make p-card purchases on behalf of the division. The use of p-card in this instance was a clear violation of the county’s FIN-1 Administrative Procedure, Accounts Payable, which states: “Procurement Card – restricted to one-time, unscheduled material and supplies purchases (no services) up to a maximum of $5,000 per transaction.”

Furthermore, we found that the vendor was on the federal Systems for Award Management (SAM.gov) excluded vendor list, meaning that the federal government had designated this vendor as one with which it would not do business. According to county management and counsel, there is no immediate exclusion to being a county contractor or vendor by virtue of placement on the SAM list, but it is up to the discretion of the purchasing manager and the PCRB rules. PCRB rules provide for the debarment (disqualification) of vendors if convicted of federal or state offenses indicating a lack of business integrity or business honesty.

However, federal funds are also subject to specific spending requirements and limitations. In this case, the payment to the SAM-excluded vendor was initially coded as being made with CARES Act and other federal funding. Payment should not have been made to the vendor with federal funding, as they were a federally suspended provider and county-identified inactive provider due to the Oregon Department of Justice investigation.

Since the transactions with the vendor were inconsistent with the county’s policy disallowing p-card purchases toward professional services, the contractor was a federally suspended provider, and the county identified this provider as inactive due to fraud investigation and ultimately conviction related to health care billing, this vendor’s payments should not have been charged to the CARES Act and other grants.

County management notified the vendor, stopped services, and continued the inactive status in Workday once final payments made for services incurred. Management also provided a reminder to the employees involved in the transactions to follow county policy that a p-card should never be used to pay for services, and that p-card privileges could be revoked for not following county policy. County management subsequently removed most of the expenses from federal pandemic-related grants, CARES Act, and charged them to county general funds. Total charges for this vendor to general funds are $6,825. Management indicated they are satisfied that the services were actually performed and that the program indicated they reviewed the invoices and supplier support for the services received.

Approval controls for a provider organization’s invoice were not followed in one instance

Through our review of provider organizations’ invoices, we identified one mispayment to a provider. An invoice was submitted by one provider to the Health Department but the county paid the amount due to another provider. The invoice clearly identified the provider, the invoice was electronically scanned and labeled with the correct provider’s name, and the scanned invoice was then loaded into the county’s financial system (Workday) where it was submitted for payment – to the incorrect vendor. The transaction went through three layers of review without any of the reviewers flagging that the provider to be paid was different from the provider on the invoice.

We notified management immediately. Management took immediate action to develop a plan to address the issue and notified upper department leadership and the Chief Financial Officer of the issue and intended actions.

Based on our review of many invoices, we believe this was an isolated incident and were satisfied that management took quick and reasonable action. However, it is of concern that an invoice could make it through so many levels of approval without adequate review of the backup documentation that is readily available. Therefore, we recommend that the department evaluate the employees assigned to approval roles to ensure their workload capacity is appropriate to effectively and adequately review transactions before completing an approval step in Workday.

Some provider organizations reported positive experiences working with the county to distribute pandemic funding, but also reported barriers to eligibility for some community members and not enough funding to go around

As part of our audit, we conducted a survey of provider organizations that received pandemic-related funding from the county to provide services and direct financial assistance to community members. We developed and issued a survey to learn how effective this funding was from the providers’ perspective, and whether there were barriers to distributing the funding to community members. We also asked questions about working with the county from an administrative point of view.

Ideally, we would have connected with community members directly about their experience, but we elected not to do in-person visits as we felt it would pose an unnecessary risk of COVID-19 infection to provider staff, their clients, and our staff. Additionally, the survey allowed us to provide an opportunity for all providers to respond to our survey versus in-person visits with just a sample of providers and their clients.

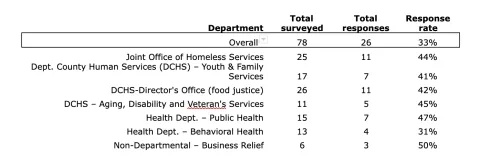

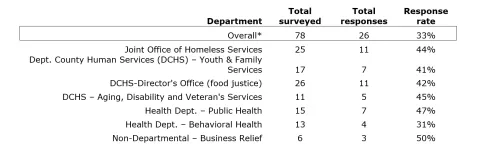

We issued the survey to providers that received pandemic net funding amounts of $25,000 or more for a combination of programs/services: business relief funds, food, housing/shelter, and/or provider services during the period of July 2020 through February 2021. We issued the survey to 78 unique email addresses for persons that represented 67 different providers. Some providers had more than one program funded by the county and worked with more than one county department. Of the 78 emails to whom we sent the survey, 26 responded, a 33% response rate. Of the 26 responses, 22 (85%) reported that the resources their organization received from the county supported a culturally specific population and/or Black, Indigenous, and People of Color community members.

Based upon the responses we received, we found that providers generally had positive experiences working with the county, but some reported barriers to eligibility for community members to receive assistance and that there was not enough funding to go around.

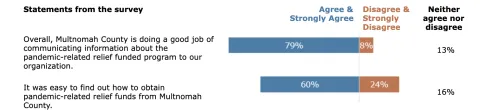

Provider organizations reported receiving good support from the county in terms of communication and speed of delivery of funding. Survey results indicate partners had some difficulty learning about how to obtain pandemic funds.

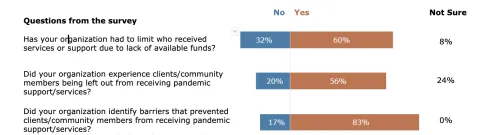

Provider organizations reported having to limit who received services or support, community members being left out of services, and barriers that prevented community members from receiving support.

For providers that said their organization experienced community members being left out from receiving pandemic support or services, we asked them to explain.

Selected comments

- As much as we tried to get the information out, some people did not request funds until the spend down was almost done.

- Rent assistance requirements have been a big barrier for many in our community. Chasing down W9, formal lease agreements (when many are informal) has left people out of support.

- Some clients who have unique living situations often were left without rent assistance due to the required paper work.

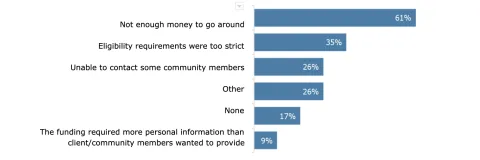

In terms of barriers that prevented clients and community members from receiving pandemic services, partners provided additional information in open-ended survey questions. We asked the question, “What barriers did your organization identify as preventing clients/community members from receiving pandemic support/services? Select all that apply.”

Nearly two thirds of those responding to the question about barriers indicated that there was not enough money to go around.

For the providers that selected “other”, we asked them to specify.

Selected comments

- Timely documentation gathering for clients - like their landlord took long to complete W-9

- Lack of staff capacity and technology challenges

- The requirements of the funds and the staffing need to facilitate

- CBO's [community-based organizations] were expected to absorb all costs for distribution of funding and given documentation requirements, this was unreasonable

- Homelessness or disability preventing people from following through or being reached

Since a good deal of direct assistance was distributed by providers, we thought asking providers how timely they received funding from the county would shed some light on the county’s ability to distribute assistance quickly. We asked providers whether the county distributed pandemic funding in a reasonable amount of time. Seventy-six percent of those who responded to the survey said that the county provided funding in a reasonable amount of time. We chose to leave the question of “reasonable amount of time” open for interpretation by the providers. We left it open for interpretation due to different programs being funded and an expectation could be different based on the program itself.

Three quarters of respondents to the survey said the county made funding available within a reasonable amount of time

We also asked providers if they had any additional comments regarding their experience with Multnomah County. Several of these comments alluded to one of the challenges of receiving CARES Act funding, specifically – that the CARES Act did not allow the funds to be used for administrative costs, such as staff time and materials. Distributing funds can be a burden on providers because of the time and cost involved.

Selected comments:

- This really tested organizational/staff capacity. We are now seeing a huge wave of transitions due to staff burnout. We needed more indirect admin support and operational/flexible resources to do this work better.

- It has been frustrating that we are supposed to absorb all administrative costs. It also has been challenging to try and help the community, specifically with COVID…support and not having enough resources to help people quarantine etc.

- Just a thank you... this funding allowed us to give critical support to families within our community in a variety of ways.

- Organizations need capacity funds outside of cares act dollars to help with costs incurred up to and including single payer audits for exceeding $750,000 in federal funds.

County management told us that some providers turned down CARES Act funding because it did not allow for the funds to be used for administrative costs. Subsequent federal funding through the American Rescue Plan Act (ARPA) does allow for administrative costs.

Recommendations

- We recommend that Central Accounts Payable provide enhanced procurement card (p-card) training to all county staff that use and/or manage p-card transactions by December 31, 2021. We recommend this enhanced training highlight that services cannot be paid for by p-card, p-cards are not to be used to circumvent accounts payable controls, the responsibility of the review and approval roles, and emphasize the consequences of not following county policies, which include but are not limited to p-card privileges being revoked.

- We recommend the Chief Financial Officer’s office develop a centralized detective control for identifying improper use of p-card transactions. A detective control is a procedure to identify errors or problems after they have occurred. This process should be in addition to Central Accounts Payable periodic audits and include a comparison of p-card vendors to the federal Systems for Award Management (SAM.gov) list. We recommend this process be performed at least quarterly and be put in place by December 31, 2021.

- From the issuance of this report through at least the end of 2022, the County Chair and Government Relations should continue to communicate frequently with Oregon's state legislature and federal delegation about rent assistance requirements that were barriers to helping people in need, particularly Black, Indigenous, and People of Color community members, receive assistance during the COVID-19 pandemic.

- We recommend that by December 31, 2021 the Health Department evaluate the employees assigned to approval roles to ensure their workload capacity is appropriate to effectively and adequately review transactions before completing an approval step in Workday.

- We recommend that by December 31, 2021 the Health Department enhance their detective controls to ensure that routine reconciliations of vendor payments are performed, to help identify any mispayments, such as monthly contract reconciliations of vendor invoices for what has been paid compared to what has been invoiced, to date.

Objectives, Scope, & Methodology

The objectives of this audit were to:

- Determine what pandemic-related relief funds the county has received or is eligible to receive in fiscal year 2021 (FY2021) and where the county spent FY2021 pandemic-related relief funds.

- Determine if policies and procedures are in place for managing the level of pandemic funding distributed by the county.

- Determine if the county made efforts to distribute FY2021 pandemic funds in alignment with the county’s commitment to leading with race.

- Determine if federal, state, and county contracting policies were followed for FY2021 pandemic funds passed onto other entities.

- Determine if policies and procedures are in place for managing supplies and inventory related to the pandemic during FY2021.

- Review allowability for some expenditures under federal, state, and/or county guidance and that there is adequate backup documentation.

- Conduct a survey of county contractors that received funding from the county specifically for pandemic-related purposes.

To accomplish these objectives we:

- Reviewed all county expenditures coded as pandemic-related for FY2021;

- Reviewed all pandemic-related revenues recognized in FY2021;

- Reviewed all pandemic-related budgeted amounts for FY2021 including all Board of County Commissioners’ Board Resolutions related to budget modifications during the fiscal year;

- Conducted over 20 interviews;

- Created a key index to document policies and procedures related to procurement, contracting, purchasing, and inventory management;

- Reviewed contracts and supporting documentation;

- Reviewed emergency procurement authorizations (waivers from competitive procurements);

- Conducted a survey of provider organizations that received pandemic-related funding from the county.

Internal Controls Scope of Work

We obtained an understanding of how the county designed contract procurement, purchasing, and inventory policies and procedures as it relates to internal controls. We conducted interviews, reviewed county policies and authoritative literature, and performed walk-throughs of processes. We analyzed specific risks of contracts, purchasing, and inventory and determined whether county policy addressed those risks.

Based on our understanding of internal controls and survey results, we assessed the effectiveness of internal control design and, to some degree, implementation. Our assessment identified concerns related to county procurement card controls. We also noted controls to have been intentionally relaxed due to the emergency declaration.

Internal Control Components and Principles

The following are the internal control components and underlying principles that are significant to the audit objective. Management is responsible for all of these activities.

Risk Assessment

- Define objectives clearly to enable the identification of risks and define risk tolerances.

- Identify, analyze, and respond to risks related to achieving the defined objectives.

- Consider the potential for fraud when identifying, analyzing, and responding to risks.

- Identify, analyze, and respond to significant changes that could impact the internal control system.

Control Activities

- Design control activities to achieve objectives and respond to risks.

- Design the entity’s information system and related control activities to achieve objectives and respond to risks.

- Implement control activities through policies.

Information and Communication

- Use quality information to achieve the entity’s objectives.

- Internally communicate the necessary quality information to achieve the entity’s objectives.

- Externally communicate the necessary quality information to achieve the entity’s objectives.

Monitoring

- Establish and operate monitoring activities to monitor the internal control system and evaluate the results.

- Remediate identified internal control deficiencies on a timely basis.

Data Reliability

For this audit, we analyzed personnel and/or financial data for the time period of July 1, 2020 through June 30, 2021 from Workday, the County’s enterprise resource planning system. Based on the annual review of Workday datasets by the County’s external auditor, and our reconciliation of data, our office has determined that the data were sufficiently reliable for the purposes of this report.

Survey of Provider Organizations

We conducted a survey of provider organizations to gain an understanding of the experiences of providers who have received pandemic-related relief funding from Multnomah County. We utilized SurveyMonkey, an online survey software that helps create surveys and collect data, as the platform for our survey. We issued the survey to providers that were identified to have pandemic net amounts of $25,000 or more for a combination of program/services of: business relief funds, food, housing/shelter, and/or provider services during the period of July 2020 through February 2021. We issued the survey to 78 unique email addresses for persons that represented 67 different providers. Some providers had more than one program funded by the county and worked with more than one county department.

The survey was conducted between May 18 and June 4, 2021. The survey was voluntary but not anonymous. We obtained a response rate of 33%.

We analyzed results by type of funding received and by department funded and found little to no significant variation in results, in most cases. Results are presented based on all responses provided; no individually identifying information is reported. The survey included mostly closed-ended questions about provider experiences. To ensure the quality and reliability of the survey, we pretested the questionnaire with auditors not assigned to this phase of the audit and requested feedback from department management for each department with providers being contacted. We conducted the pretests to check (1) the clarity and flow of the questions, (2) the appropriateness of the terminology used, and (3) if the survey was comprehensive and unbiased. We revised the questionnaire based on the pretests. Our office determined the data were sufficiently reliable for the purposes of this report.

Statement of Compliance with Government Auditing Standards

We conducted this performance audit in accordance with generally accepted government auditing standards. Those standards require that we plan and perform the audit to obtain sufficient, appropriate evidence to provide a reasonable basis for our findings, and conclusions based on our audit objective. We believe that the evidence obtained provides a reasonable basis for our findings and conclusions based on our audit objectives.

Audit Staff

Annamarie McNiel, CPA, Principal Auditor

Marc Rose, CFE, Principal Auditor