What we found

The Auditor’s Office follows up on audit recommendations to support county government’s accountability.

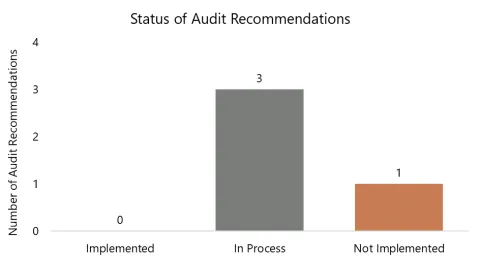

We found that the county is in the process of implementing three recommendations and has not implemented one recommendation from the 2023 budget process audit.

What the statuses mean

- Implemented – Auditee has fully implemented, or auditee has resolved the issue to meet the recommendation’s intent.

- In Process – Auditee has started implementation.

- Not Implemented – Auditee has not implemented, or does not intend to implement.

Recommendations in process

Recommendation #1: To improve transparency, the Budget Office and Chief Financial Officer should develop an administrative procedure requiring all county departments to report to the Board of County Commissioners at least once each fiscal year on revised budget to actual expenditures at the foundational unit of the county's budget, which is currently the program offer level.

Auditor’s Note: Based on inquiry with the Budget Office, they are working with the Chief Financial Officer to develop a new policy that will be part of the fiscal year (FY) 2026 budget process. Per the Budget Office, this new policy will outline the requirements for reporting budget to actual expenditures at the program offer level. These new policies and guidelines will be included in the FY2026 Financial and Budget Policy that the Board of County Commissioners adopts as part of the annual budget process.

The Budget Office has rolled out a monthly budget monitoring dashboard that reports actual expenditures at the program offer level and shows how they compare to budgeted expenditures. These dashboards are publicly available on the Budget Office’s website.

We are considering this recommendation in process, since the new policy is not yet in place.

Recommendation #3: The Chair should direct the Budget Office and departments to engage community budget advisory committees earlier in the budget process and provide them with information sooner, so their comments have more time to be addressed with the release of the Chair’s proposed budget.

Auditor’s Note: Under the Chair’s direction and a Commissioner’s FY2025 Budget Note, the Office of Community Involvement held several listening sessions with members of the Community Budget Advisory Committees (CBACs) and CBAC coordinators to assess the needs and challenges the CBACs face in the budget process.

From this work with the CBACs, the Office of Community Involvement drafted a CBAC Improvement Plan and proposed county code changes. These drafts were shared with the Board of Commissioners at the September 24, 2024 board briefing. The Office of Community Involvement has also drafted a CBAC timeline. Based on our inquiry, the timeline is intended to assist CBAC staff and volunteers by providing them with key milestones and actions for their work and by outlining the scope of their work and its links to the larger budget process.

We are considering this recommendation in process, because most of the efforts described above are currently in draft form and are intended to be implemented as part of the FY2026 budget process.

Recommendation #4: The Board of County Commissioners should study whether the county should budget on an annual or biennial process and report on the results of this study. Areas to study could include potential impacts on community involvement in the budget process, budget inputs and outcomes, and monitoring of adopted budget to actual expenditures.

Auditor’s Note: The Budget Office hosted a Hatfield Resident Fellow through Portland State University to research the advantages and disadvantages of a biennial budget process and wrote a report. The report does not provide a recommendation but rather context for further consideration by the County. In November 2024, the Chief Budget Officer provided a copy of the report to the Board of Commissioners for their review.

We are considering this recommendation in process because this recommendation is directed at the Board of County Commissioners to study the option of a biennial process. While the Commission has received a copy of the report, they received it recently. Additionally, a majority of the Board of Commissioners is set to turnover by January 2025. The new commissioners should be allowed the opportunity to study these results given the short timeframe for the current commissioners to adequately review results and consider their impact before this turnover.

Recommendations not implemented

Recommendation #2: To improve transparency, the Board of County Commissioners should develop a policy requiring departments to report to them when they intend to make expenditures in a way that the Board defines as materially different than how they proposed to spend funds in program offers.

Auditor’s Note: We are considering this recommendation not implemented as of the date of this report.

As noted in the response to Recommendation #1, the Budget Office has rolled out dashboards to report on budget to actual expenditures. Additionally, the new Financial and Budget policy, noted in Recommendation #1, is expected to include reporting guidelines for departments to report to the Board of County Commissioners on substantive differences between budget and actuals. The Budget Office is currently putting this recommendation on hold until they have an opportunity to study the impact of the new policy and reporting so the Board can be better informed when it comes to developing a policy that defines “materially different.”

Objectives, scope, & methodology

The objectives of this evaluation were to determine the status of recommendations from the 2023 Multnomah County Budget Process Audit: County needs better reporting on expenditures and more time for community involvement that had a due date of September 30, 2024.

Auditors evaluated the status of recommendations based on interviews, documentation, and other available evidence.

Updating the status of a recommendation

During each audit our office conducts, we develop recommendations intended to improve government operations, particularly with regard to effectiveness, transparency, accountability, and equity. Our goal for evaluating the status of recommendations is to help ensure management implements these recommendations for improvement.

We recognize that after we publish an evaluation on the status of recommendations, management may fully implement a recommendation that we reported was in process or not implemented. Management can then provide evidence to the Auditor demonstrating why the recommendation’s status should be changed in the Auditor’s future reporting. The final decision on whether to change any recommendation’s status rests with the Auditor.

Staff

Annamarie McNiel, CPA, Operations & Audit Director