On this page

- Report Highlights

- Background

- The county's contract monitoring policy is outdated and not being used

- The county cannot fully and adequately evaluate if it is making timely payments to providers

- There are opportunities for better coordination between county offices

- Recommendations

- Scope, Objectives, & Methodology

- Audit Staff

- Related documents

Report Highlights

A consistent countywide approach is needed to contract monitoring.

- What we found: Outdated contract monitoring policy led to a lack of countywide standards, which resulted in varying practices among departments.

- Why this is important: Evaluating county contracted programs consistently and equitably helps to ensure contracted providers effectively deliver community services.

- What we found: The county cannot fully and adequately evaluate if it is making timely payments to providers.

- Why this is important: Providers rely on timely payments. The county has a responsibility to ensure it is meeting its obligations to providers.

- What we found: There are opportunities for better coordination between county offices.

- Why this is important: Improving effectiveness and efficiency of practices reduces the risk of duplicating efforts and wasting resources.

Background

Contract monitoring ensures that community members have access to critical health and human services

Multnomah County had a budget of more than $1.2 billion in contractual services for fiscal year 2023 (July 1, 2022 to June 30, 2023) contracts. A large portion of those contracts were health and human services contracts between the county and contracted service providers (providers) that aim to deliver essential services to our community members, like behavioral healthcare and housing assistance. The COVID-19 pandemic challenged the county's ability to deliver such essential services to our community and stressed the importance of the county's partnerships with providers.

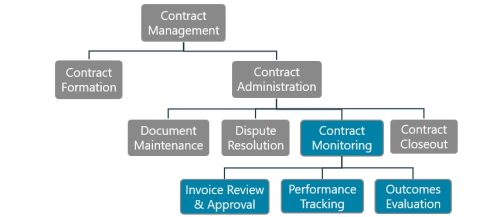

The overarching process of contract management is made up of two functions, contract formation and contract administration. Contract formation occurs before a contract is signed by the county and a provider. It involves operations like developing the solicitation, formulating the scope of work, and negotiating the terms and conditions of the contract. Contract administration occurs after a contract is signed by the county and a provider. It involves operations like maintaining documents, resolving disputes, contract monitoring, and closing out the contract at the end of its lifecycle.

This audit focused on contract monitoring activities

In this audit report, contract monitoring refers to the processes and procedures that Multnomah County uses to verify whether the county and providers are meeting contract terms and performance measures. Contract monitoring should involve mechanisms for the county to track the services that providers deliver and their performance, measure program effectiveness, and resolve problems that may arise. Typical contract monitoring tasks include reviewing and approving invoices prior to paying them, tracking the performance of providers, and evaluating performance outcomes.

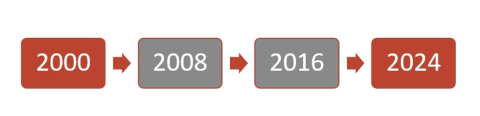

Contract monitoring recommendations from our office span 24 years

Prior audits addressed contract monitoring, but the county only implemented some recommendations

The Auditor's Office has highlighted the necessity of contract monitoring in our audits throughout the past 24 years. We wrote about contract monitoring issues in the

audit of 2000. This audit found that some departments could strengthen fiscal and program monitoring by adopting best practices.

Eight years later, our office revisited the subject again in the

audit of 2008. This audit found that many vulnerable clients are served through complex contracts that are challenging to manage, and that when viewed as a system, the county lacked a strategic, risk-based, organization-wide approach to contract monitoring.

After another eight years, the

of 2022 identified waste of county resources of more than $525,000 due to ineffective contract monitoring, which resurfaced the significance of contract monitoring and led the Auditor's Office to revisit the subject in this audit.

Countywide redesign and standardization of contract administration has begun

The Department of County Management is leading a countywide contract administration standardization effort, which includes contract monitoring. During fiscal year 2023, the department hired a third-party consultant to identify opportunities for improvements in Multnomah County's procurement and contracting systems. The results of that review distinguished contract administration as an area requiring further development and alignment with best practice throughout the county.

In fiscal year 2024, the department created a new business unit housing two positions within Central Purchasing to update the purchasing and contracting organizational model. This unit is charged with advancing the work of carrying out recommendations from the third-party consultant's report in a multi-year plan. Additionally, in February 2024, the Department of County Management's purchasing team completed a Strategic Contract Administration Assessment, focused on only one county department, to determine which aspects of contract administration are already in place. Our audit determined to what extent contract monitoring activities are occurring and whether equity factors are being considered in those activities at the department, division, and program level.

Recommendations can help improve monitoring countywide

We analyzed contract monitoring best practice resources from the National Institute of Governmental Purchasing and the National Association of State Procurement Officials, which informed the criteria for evaluating county processes and procedures in this audit.

We considered the following best practices in contract monitoring:

- Document contract monitoring policies and procedures

- Monitor contract performance.

- Ensure providers achieve milestones and meet timelines.

- Track outcomes.

- Review and approve invoices prior to payment.

- Reconcile invoices against services provided.

- Conduct site visits, inspections, and testing.

- Hold regular meetings between the county and providers.

- Review providers' performance and follow up on action items.

- Report on status, activity, and compliance deliverables.

- Manage contract compliance.

- Address nonperformance, noncompliance, and breaches of contract.

The scope of this audit focused on contract monitoring of health and human service contracts during the life of the contract. We selected the Joint Office of Homeless Services, Department of County Human Services, Health Department, and Department of Community Justice for sample testing, because they are the four departments that enter into the most health and human service contracts. We tested invoice payments made to a sample of providers, looked for evidence of monitoring conducted by county staff, and surveyed the providers whose contracts were selected for testing. We did not include procurement activities, contract formation operations, or other contract administration operations in our audit scope.

It is important to note that Multnomah County uses many other types of contracts, such as intergovernmental contracts, capital projects (construction) contracts, and information technology (IT) contracts, to name a few. It is reasonable that contract monitoring activities and resources may vary throughout the county due to the different needs and constraints presented not only within each contract type but also among the departments, divisions, programs, and providers that enter into these contracts. However, a level of standardization and coordination throughout the county could improve efficiency and effectiveness of contract monitoring by providing clear expectations and consistent procedures. While this audit is related specifically to health and human service contract monitoring at four county departments, the recommendations of this audit can assist in improving contract monitoring of other contract types countywide.

Acknowledgment

We appreciate all department staff and leaders who participated in this audit. We are also grateful to service providers who responded to our survey. We recognize that both the county and providers share a common goal in supporting the Multnomah County community to the best of their abilities. We value their contributions and the time they shared with us.

As expected, providers, departments, and divisions were profoundly impacted by the COVID-19 pandemic. A couple county staff shared additional context with us about the impact COVID-19 had on them, which is significant, traumatic, and ongoing. Additionally, there was a significant increase in contract spending in fiscal year 2023. Providers that responded to our survey also noted issues with county staff turnover and shortages which had an impact on doing business with the county. Our testing, focused on fiscal year 2023 and early fiscal year 2024, revealed inconsistencies in contract monitoring. For example, one division was found to still be rebuilding contract monitoring systems after significant strain on resources, and a different department was redesigning contract monitoring tools and processes to be more relevant, efficient, and effective.

The county's contract monitoring policy is outdated and not being used

The county is not applying contract monitoring practices consistently or equitably across providers

Policies and procedures are fundamental to the operations of an organization as they help ensure compliance with laws and regulations and provide important information that facilitates decision-making. A standard countywide framework that reflects the current county needs can help the county evaluate programs consistently, treat providers in an equitable manner, and ensure providers are delivering contracted services.

The county has a policy called Multnomah County Human Services Contract Administration - Contract Monitoring. The policy is intended to be countywide for human services contracts, unless a department has a more stringent policy in place. The policy states that "Contract monitoring ensures that all contractors are in compliance and providing the services that are being purchased." The policy covers detailed requirements for annual assessments, invoice monitoring, program monitoring, reporting on the monitoring, follow-up action plans, and delivering the reporting results to providers.

This policy has not been updated since 2011. In our interviews, we found that some departments' leadership knew about the countywide policy, but some program staff responsible for monitoring contracts were not aware of it. This was likely a reason we found inconsistent monitoring practices among departments and even among divisions within departments. In some cases, individual program staff determined how to best monitor programs. We did find that a couple departments and a division had their own documented department/division-level contract monitoring policies, but even one of those policies was outdated and not in effect.

Divisions and departments had inconsistent monitoring practices, creating risk that contracted services were not provided

Health and human services programs that the county contracts for are typically unique from department to department and even between programs. But, the lack of consistency in contract performance monitoring creates risk that the contracted services are not delivered to the community. For example, if on-site observations are not being performed the county may not be responding timely to situations where a provider is out of compliance or not performing services.

Departments have a wide variety of programs and program needs, so it is reasonable to expect that not all contracts would be monitored exactly the same way. However, the inconsistency in applying a countywide contract monitoring policy can lead to gaps in monitoring, especially when there is staff turnover. The lack of a consistently applied policy can lead to frustration on the provider side as many providers have several contracts with multiple county departments, divisions, and programs within divisions.

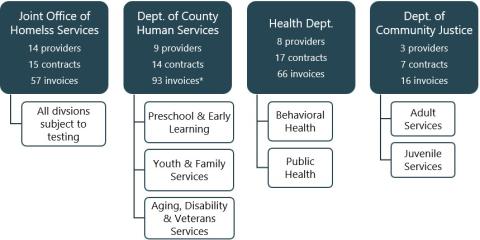

We tested a sample of contracts for four departments: Joint Office of Homeless Services, Department of County Human Services, Health Department, and Department of Community Justice, focusing on divisions within the departments that had significant health and human services contracts. For the Joint Office of Homeless Services, all divisions were subject to testing. For the Department of County Human Services, we tested a sample of contracts under three divisions: Preschool & Early Learning; Youth & Family Services; and Aging, Disability, & Veterans Services. For the Health Department, we tested a sample of contracts for two divisions: Behavioral Health and Public Health. For the Department of Community Justice, we tested a sample of contracts for two divisions: Adult Services and Juvenile Services.

County departments and divisions that we selected a sample of for testing

Note: Some providers included in our testing had contracts with more than one department.

*We sampled more invoices for the Department of County Human Services, because some Youth & Family Services providers bill several invoices per month for their various programs.

Overall, our testing revealed that each department or division conducted some level of contract monitoring. For each department, we tested a sample of invoices for approval. We found that all 232 invoices we tested had approval and that an appropriate person(s) approved the invoice. However, monitoring of contract performance was inconsistent among the departments and divisions we tested.

We found that departments and divisions are monitoring contracts, but not all monitoring was the same

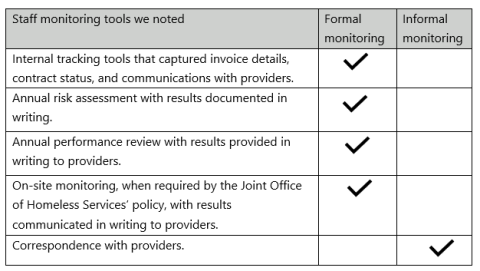

We considered the various monitoring activities performed by departments to be formal or informal. Formal monitoring helps increase the likelihood of consistent application of tools across providers, which helps ensure providers are delivering contracted services. We considered formal monitoring to be tasks such as risk assessments, performance reviews, and on-site monitoring that was documented with written letters or memos (both internally and communicated to providers). We also considered the use of internal tracking tools that captured specifics such as invoice details, contract status, and communications with providers as a formal monitoring tool. We considered informal monitoring to be tasks such as correspondence with providers that was documented with email or calendar appointments showing the attendance of meetings or on-site observations not formally documented in letters or memos.

The Joint Office of Homeless Services and the Department of County Human Services' Youth & Family Services Division had the most evidence of formal monitoring for the sample of contracts we tested

- Department: Joint Office of Homeless Services

- Division: All

- Monitoring occurring? Yes

- Type of Monitoring: Formal & Informal

- Department: Department of County Human Services

- Division: Preschool & Early Learning

- Monitoring occurring? Yes

- Type of Monitoring: Mostly Informal

- Department: Department of County Human Services

- Division: Youth & Family Services

- Monitoring occurring? Yes

- Type of Monitoring: Formal & Informal

- Department: Department of County Human Services

- Division: Aging, Disability, & Veterans Services

- Monitoring occurring? Yes

- Type of Monitoring: Mostly Informal

- Department: Health Department

- Division: Behavioral Health

- Monitoring occurring? Yes

- Type of Monitoring: Mostly Informal

- Department: Health Department

- Division: Public Health

- Monitoring occurring? Yes

- Type of Monitoring: Mostly Informal

- Department: Department of Community Justice

- Division: Adult Services

- Monitoring occurring? Limited

- Type of Monitoring: Informal

- Department: Department of Community Justice

- Division: Juvenile Services

- Monitoring occurring? Limited

- Type of Monitoring: Informal

Source: Auditor's Office

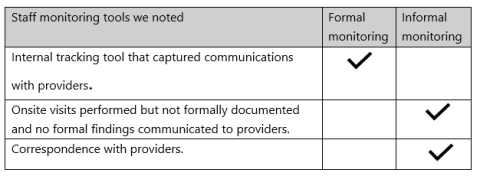

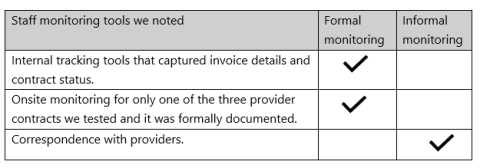

Joint Office of Homeless Services staff conducted formal monitoring activities, documented them, and applied them consistently

The Joint Office of Homeless Services has department-level contract performance monitoring policies in place.

For each Joint Office of Homeless Services contract we tested we noted the following:

The Department of County Human Services contract performance monitoring was unique to each division

The county created the Preschool & Early Learning Division in response to the voter approved "Preschool for All" measure in November 2020. The division began contracting with providers the following budget year (fiscal year 2022). It was still a relatively new program during the period we tested of fiscal year 2023 and the first part of fiscal year 2024. The division was still finalizing formalized monitoring processes and tools and expected to roll out the tools for providers starting in early 2024, which was beyond the period we specifically tested. While the division was still finalizing these formal processes and tools, we did find evidence of monitoring occurring that was more informal.

For each Preschool & Early Learning Division contract we tested we noted the following:

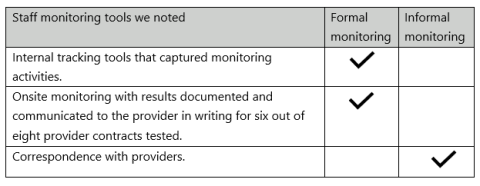

The Youth & Family Services Division had formal monitoring processes in place including division-level contract performance monitoring processes.

For each Youth & Family Services Division we tested we noted the following:

On-site monitoring for two of the eight provider contracts tested had not had a site visit since 2018. Division staff shared that part of this was due to disruption from the pandemic as well as that the program specialist managing the program was out on leave during fiscal year 2023.

For the Aging, Disability, & Veterans Services Division, we found that some monitoring was occurring, but found their monitoring was informal and left to the discretion of the program staff managing the program under the contract.

For each Aging, Disability, & Veterans Services Division contract we tested we noted the following:

The Health Department monitoring was unique to each division we tested

The Health Department contract performance monitoring was unique for each division and even varied among programs within divisions. We found that some monitoring was occurring but found their monitoring was informal beyond capturing data on internal tracking tools.

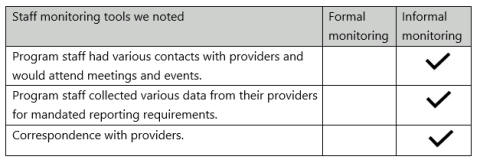

For the Behavioral Health Division contracts we tested we noted the following:

For the Public Health Division contracts we tested we noted the following:

The Department of Community Justice conducted limited monitoring

The Department of Community Justice had limited monitoring and did not conduct performance monitoring of their providers during the period we tested. It is worth noting that some of the Department of Community Justices services are performed on-site at county buildings so the county is aware of the providers' presence with services but there is no formal monitoring of the services being provided. While they have a department-level contract monitoring policy, it has not been updated since 2009. Additionally, staff informed us that the policy is not being used.

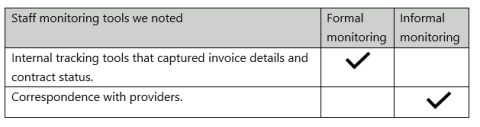

For the Department of Community Justice contracts tested, we noted the following:

However, the Department of Community Justice told us that they were working on a new contract review process during our audit. We were able to confirm that the department has a workgroup developing their new contract review process and, as of the writing of this report, department management indicated they were working to roll out the new process to program staff. We found that the department's monitoring of the contracts we tested for fiscal year 2023 was limited to invoice reviews and informal oversight, which varied among program staff. By not having an updated policy in place and enforced, staff are performing monitoring tasks at their own discretion. This can lead to inconsistent monitoring of providers and risk of providers not delivering contracted services.

The county cannot fully and adequately evaluate if it is making timely payments to providers

Invoice due dates are likely to be inaccurate in the county's billing system

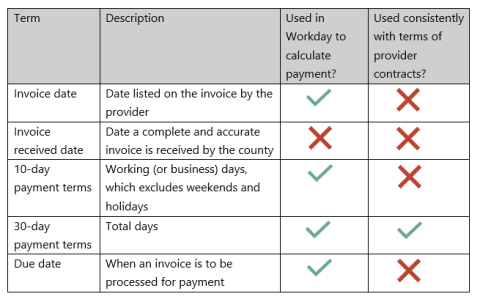

Most of the county's contracts with providers describe how and when the county will process payment to the provider for services provided. Some older contracts do not specifically state the terms for payment. For contracts that do not state specific payment terms, the county applies a 30-day default term.

For the contracts we tested, the Department of County Human Services' and the Joint Office of Homeless Services' contracts define that payments will be processed within 10 working (or business) days, which exclude weekends and holidays, of receipt of a complete and accurate invoice. The Health Department and Department of Community Justice have 30-day terms for their contracts, which refer to total days. When an invoice is to be processed, it is referred to as an invoice's "Due Date."

A contract's payment terms are used to establish the terms set up in Workday, the county's financial system that facilitates payments to providers. The noted payment terms for our sample were accurate in Workday in all cases except for one provider, where their terms were 10 days in Workday but 30 days in their contract.

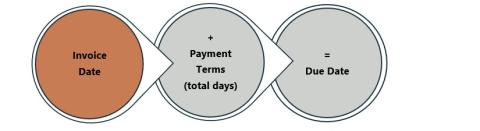

However, Workday calculates an invoice's "Due Date" based on a manually entered "Invoice Date." This "Invoice Date" is from the provider-submitted invoice. Additionally, an invoice's due date is calculated using total days for both 10 working days and 30-day payment terms. This is not consistent with payment terms outlined in county policy or most of the provider contracts we tested, which indicate payment is due based on when a complete and accurate invoice is received.

County is not using Workday consistently with provider contract terms

Currently, the due date is the sum of the date stated on an invoice and payment terms under the contract

The current due date calculation is problematic for a couple of reasons:

- The Invoice Date does not necessarily indicate when the county received an accurate and complete invoice. Our sample revealed that the county received 84% of invoices after the "Invoice Date" listed in Workday. This makes the calculation inaccurate for any invoice with an "Invoice Date" that is different from the date the county received a complete and accurate invoice.

- The due date is calculated using total days and does not account for weekends or holidays. This makes the calculation inaccurate for any contract with payment terms of 10 working days.

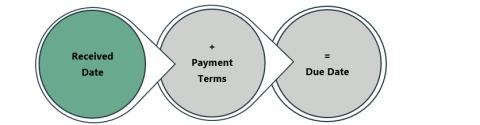

The due date should be the sum of the date the county receives an invoice and payment terms under the contract

Workday is set up to capture an invoice's "Received Date," which should be the date the county receives a complete and accurate invoice. However, "Received Date" is currently not used to calculate the invoice due dates. Additionally, the "Received Date" entered into Workday is typically the date the department's Accounts Payable unit received the invoice. It is not necessarily the same date the county received a complete and accurate invoice from the provider.

In our sample, the county received 73% of invoices on a date other than what was noted in Workday as the "Received Date." This is because an invoice is often received first by department staff with firsthand knowledge of the work performed. They review and approve the invoice before sending it to their department's Accounts Payable unit for final review, approval, and payment.

It is challenging to capture an invoice's complete and accurate received date because it relies on county staff to manually enter a date that the county has not defined well. If an invoice is received but requires follow-up with the provider (questions, corrections, or additional support requests) it could make the exact date difficult to determine. For example, a program-level staff may work with a provider to get a complete and accurate invoice before forwarding it to a department's Accounts Payable unit for payment. It is often the departments' Accounts Payable staff who interface with Workday and not always a program staff person. Capturing an accurate received date and getting it entered into Workday would require changes to current processes.

Providers may also have a different idea of what a received date means (first received by the county or after follow-up questions) and when it starts the clock for determining invoice due dates. We surveyed the providers whose contracts and invoices we tested, and one provider asked to meet with us to share additional context to our survey questions. This provider asked for clarity on whether the payment should be 10 days after the county receives the invoice or 10 days after county staff review. Ensuring providers have clarity on this distinction can help providers have clear expectations on when payments are due.

By not using the date an accurate and complete invoice is received to calculate the "Due Date", it is likely to be inaccurate. Therefore, the county cannot adequately evaluate if it is making timely payments to providers.

Timeliness of payments varied among departments and even among divisions within departments

Providers rely on timely payments. Most of the contracts we tested are cost reimbursement, meaning the provider already incurred the costs they are seeking reimbursement for. It can be challenging to meet financial obligations such as payroll if payments are delayed. When payments to contracted providers are delayed, the county risks disrupting services to the community, ultimately risking disruption to services the county relies on providers to deliver.

As noted above, provider contracts describe the payment terms. For the contracts we tested, the terms were either 10 working days, 30 days, or the county's 30-day default terms if not specifically detailed.

We tested a sample of 232 invoices for timeliness of payment. We obtained support from departments to determine each invoice's received date, such as the date a final invoice was emailed by the provider to the county. If an invoice required correction, we used the date the final corrected invoice was received. We then calculated the days it took to pay the invoice and then compared those results against the identified contract payment terms.

Based on the sample of invoices we tested, we found that the timeliness of payments varied greatly among departments and even among divisions within departments for the invoices tested.

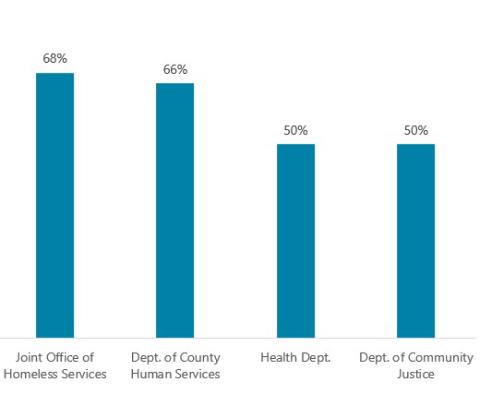

Interestingly, the departments with more stringent payment terms were making more timely payments for the invoices we tested. The Joint Office of Homeless Services and the Department of County Human Services both have 10 working days (which is typically about 14 total days) as the payment terms for the contracts tested. We found that about two-thirds of the invoices tested for Joint Office of Homeless Services and Department of County Human Services were paid on time and within the contract's payment terms. The Health Department and Department of Community Justice both have 30 days as the payment terms for the contracts we tested. We found that only 50% of the invoices we tested for the Health Department and Department of Community Justice were paid on time and within the contract's payment terms. As we previously noted earlier in the report we tested 57 invoices for the Joint Office of Homeless Services, 93 invoices for the Department of County Human Services, 66 invoices for the Health Department, and 16 invoices for the Department of Community Justice.

The Joint Office of Homeless Services and Department of County Human Services were better at paying invoices within a contract's payment terms

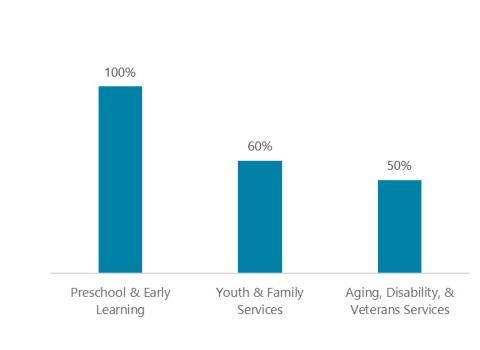

Departments have centralized fiscal staff. However, timeliness of payments can be dependent on the processes of a department's division program staff since reviews are also occurring at the division level. While we found that 66% of the invoices we tested for the Department of County Human Services were paid on time, it varied when evaluated at the division level. We tested invoices for three Department of County Human Services divisions: Preschool & Early Learning, Youth & Family Services, and Aging, Disability, & Veterans Services. While all of Preschool & Early Learning's invoices were noted to be paid within the terms of their contracts, we saw the rates for timely payments of invoices tested for Youth & Family Services (60%) and Aging, Disability, & Veterans Services (50%) were lower. We tested 14 invoices for Preschool & Early Learning, 73 invoices for Youth & Family Services, and 6 invoices for Aging, Disability, & Veterans Services.

Within the Department of County Human Services, the Preschool & Early Learning Division was better at paying invoices within a contract's payment terms

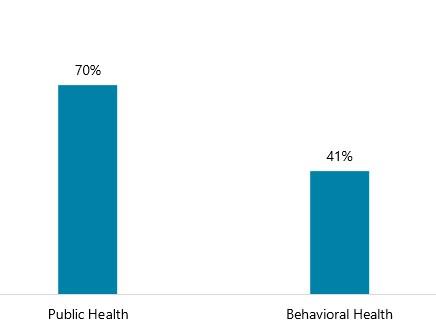

For the Health Department, division-level invoicing also varied between divisions. We tested invoices for two divisions within the Health Department: Public Health and Behavioral Health. We noted that Public Health had a majority (70%) of invoices paid on time, while only 41% of Behavioral Health's were paid on time. We tested 20 invoices for Public Health and 46 invoices for Behavioral Health.

Within the Health Department, the Public Health Division was better at paying invoices within a contract's terms

We tested invoices in two of the Department of Community Justice's divisions (Adult Services & Juvenile Services). However, due to the low dollar amount of contracts, we tested only one Juvenile Services contract, and it was on an allotment payment method (contracted monthly amount). Therefore, the results are reflected at the department-level only and, as noted above, we found only 50% of invoices were paid on time.

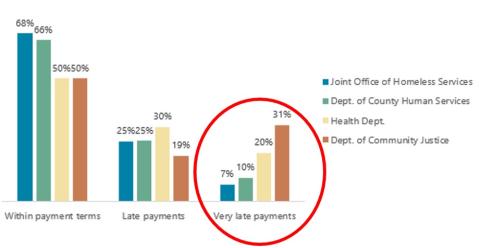

The reasons for delay in payments could be attributed to many factors. In our evaluation of timeliness of payments, we focused on invoices with "very late payments". These are identified in the red circle in the chart below.

For contracts with 10 working days, we looked more closely into the cause of delay for any invoice paid beyond 20 working days. We found 7% were delayed more than 20 working days for the Joint Office of Homeless Services and 10% for the Department of County Human Services. When looking at the division level for the Department of County Human Services we found 0% for Preschool & Early Learning, 11% for Youth & Family Services, and 17% for Aging, Disability, & Veterans Services were paid beyond 20 working days.

For contracts with 30-day payment terms, we looked more closely into the cause of delay for any invoices paid beyond 60 total days. We found 20% were delayed more than 60 total days for the Health Department and 31% for the Department of Community Justice. When looking at the division level for the Health Department we found 10% for Public Health and 24% for Behavioral Health were delayed more than 60 total days.

Almost a third of the Department of Community Justice's invoices tested were paid more than 60 days after receiving an invoice

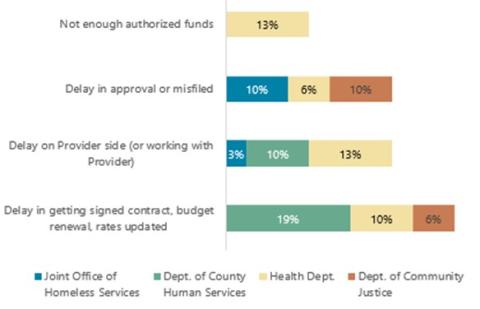

Of the 31 payments in our sample noted as being "very late payments" (red circle in the graph above), we noted that about a quarter (26%) included issues on the provider's side, such as getting their federal rate letter approved that allows them to charge indirect costs on their contracts. Indirect costs are costs that are incurred for a common or joint purpose benefiting more than one program or cost object (e.g. administration, accounting, or human resources) and not readily assignable to a specific cost object. A provider will obtain a federally approved indirect rate, or use an allowable default rate, to be applied to allowable direct costs to help recover these indirect costs.

We found that the remaining 74% of "very late payments" were due to issues within the county's control:

- 35% were delayed due to lack of a signed contract or annual budget in place, or getting rates/COLA updated before being able to process the invoice for payment.

- 26% were related to delays in the county's processing of invoices. For example, delays in approval or misfiled invoices.

- 13% related to not having enough funds authorized on the contract and needing a correction or exception to pay.

Reasons for very late invoice payments

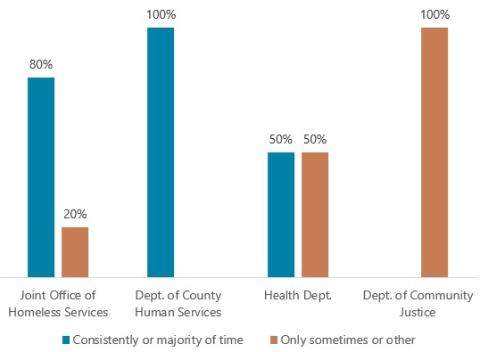

Provider perspectives on timely payment are less positive for the Health Department and the Department of Community Justice

In addition to testing invoices to determine if an invoice was being paid within the contracts' payment terms, we surveyed providers of the contracts we tested to get their perspective on how consistently their invoices were being paid. While these tests and questions are slightly different from one another, we did find our testing results were reasonably reflective of the survey results for providers who responded to the question (76% response rate). The Joint Office of Homeless Services was noted to have positive response rates among providers, while all provider responses for the Department of County Human Services indicated their invoices were being paid consistently or a majority of the time (56% consistently and 44% majority of the time). The Health Department and Department of Community Justice had less positive perspectives from the providers we surveyed.

Providers' assessments of timeliness of payments was reasonably consistent with our testing results

Note: Consistently = greater than 90% of the time. Majority of the time = between 50-90% of the time. Only sometimes = between 25-50% of the time. For those that marked Other, the response indicated issues with timeliness.

Minor corrections are holding up payments to providers

The effort and resources it can take to make a minor rounding or insignificant error correction is not efficient and takes valuable staff resources from county and provider staff.

County policy and most contract terms specifically indicate that an invoice is to be accurate and complete in order to be paid on time. However, if there is a minor inaccuracy it may be more efficient to process a payment with the minor inaccuracy than take county and provider resources to correct such an error.

We reviewed the invoices that the county processed for payment in our testing of invoices. In some cases, an invoice would require correction before it could be processed for payment. We were able to review the correspondence for some of these corrections. In general, the corrected invoices were the result of the review that required an updated invoice due to things such as incorrect amounts reported (under or over billing) or supporting documentation missing or not matching. However, some of these corrections were the result of very minor inaccuracies. Below are a couple of examples:

- An invoice was returned to a provider for a five cent ($0.05) difference on a supporting document. This invoice's total was over $396,726. The total turn-around time for this invoice from original receipt, county review, comments to the provider, and a final invoice was only three days. However, the effort and resources it took to make a 5-cent correction by both the county and provider is not efficient nor of any value.

- An invoice was first received on 10/11/2022. The county noted issues and that the provider needed to make a correction. County staff emailed the provider on 10/21/22, 10 days after receipt of the original invoice. The provider sent an updated invoice on 11/4/2022. A second issue was noted and the county requested backup for a $4.33 utility charge on 11/15/2022, 11 days after receipt of the corrected invoice. A final and accurate invoice was received on 11/15/2022. This $54,607 invoice was paid on 11/25/2022. Based on payment terms, 10 working days, the payment was considered timely because a final and accurate invoice was received and paid within 10 working days. However, the amount of time it took to process, review, and receive an accurate invoice took over a month with the final correction being for an insignificant amount (less than $5).

Based on the fact that program and fiscal staff sent invoices back for minor errors, it appears that program and fiscal staff may not know if they have the authority to override such insignificant errors. Consistent countywide training to help ensure staff have the proper information on when such an override is reasonable and allowable would benefit the county and providers.

There are opportunities for better coordination between county offices

When all parties involved in a process are aware of the roles and responsibilities of each stakeholder, it can lead to less confusion and more efficient practices. Communication and information-sharing are critical components to help ensure such a process is successful.

Federal regulations and the county's contracting policies require a fiscal compliance review if federal funding is used to fund a contract. To meet this requirement Fiscal Compliance completes required risk assessments.

Risk assessments are a tool to better understand the conditions of a provider, thereby allowing the county to know how best to support the provider. For example, if the provider is a smaller organization, they may need more support on administrative tasks such as invoicing and understanding what is and what is not allowable under the terms of their contract, or how to meet performance goals.

Fiscal Compliance's risk assessments and reviews are largely focused on fiscal evaluation of providers which includes elements of a providers' financial risks, compliance with applicable federal and state rules and regulations, and assessment of a providers' financial systems and internal controls as well as their accounting practices. The risk assessment and compliance reviews performed by Fiscal Compliance do not focus on a providers' program performance.

The Fiscal Compliance unit's risk assessment and compliance review has a very specific function and should not be used to replace a department's need to fully evaluate and monitor a provider.

Some department staff shared with us that they rely on Fiscal Compliance's risk assessment of a provider, with one program staff indicating that fiscal compliance performs the site visits. Other staff also indicated that they do not see these assessments or review results and would like to, while one department was noted to complete their own risk assessments.

While departments can benefit from the Fiscal Compliance unit's risk assessments and fiscal reviews, it's important that they do not overly rely on Fiscal Compliance's work as it could result in the department missing other areas of risk. Areas of risk are important when determining the level of oversight needed and whether a provider is meeting the required statement of work and performance goals as outlined in their contract.

The Joint Office of Homeless Services performs their own annual risk assessment and annual performance review on each of their providers independent of the Fiscal Compliance unit's risk assessment. While the Joint Office of Homeless Services' risk assessments and annual reviews include elements of fiscal evaluation, they also evaluate program services, outputs, and outcomes. The Department of County Human Services' Youth & Family Services Division also performs formal on-site monitoring to help determine whether a provider is meeting program standards and to better understand the work being performed. The Joint Office of Homeless Services and Department of County Human Services' Youth & Family Services Division reviews are performed by program staff, who have firsthand knowledge of program requirements, needs, and challenges.

While it is not appropriate for departments to replace their responsibilities for assessments and monitoring with the work done by Fiscal Compliance, there is an opportunity for better coordination between departments and Fiscal Compliance. If departments better understand what Fiscal Compliance does and does not do, they will be better informed about what is required of them. Additionally, it is critical that program staff performing the work have this information, not just managers, so the program staff are well equipped to best perform the monitoring needed.

While there is a need for both Fiscal Compliance and program-level risk assessments and monitoring, it is important that these roles are clear and well-communicated. There should be clarity and distinction between the roles, how they are carried out, and what purpose they serve. This is critical not only for county staff but also for providers. While Fiscal Compliance's role and purpose are well defined, we found that staff and providers are not always clear on the distinction between what is and is not covered by Fiscal Compliance. We found that program staff inappropriately rely on the Fiscal Compliance risk assessments and reviews, leading to gaps and inconsistencies in monitoring and confusion on the provider side.

Recommendations

We recommend that the Chief Operating Officer, no later than June 30, 2025:

- Work with departments to develop a current standard contract monitoring policy that can be used as a framework countywide.

- Develop a mechanism to evaluate department compliance with the countywide contract monitoring policy.

We recommend that the Chief Financial Officer (CFO), no later than June 30, 2025:

- Evaluate the inputs into Workday that drive an invoice's "Due Date" to help ensure this date can be used to evaluate the county's compliance with provider payment terms.

- Develop a mechanism to evaluate department compliance with provider payment terms.

- Develop training and information tools for both county program staff and managers and service providers so that there is consistency of information being shared. It is important that information and training are provided consistently and to those performing the contract monitoring tasks. We recommend this take the form of an annual symposium (or similar) and that it includes information sharing on:

- the tasks and expertise the CFO's Office supports

- limitations of the CFO's Office supports

- updates to policies, standards, and regulations impacting contract monitoring

- new or emerging issues

Scope, Objectives, & Methodology

Health and human services contracts make up one of the main areas of contracting at Multnomah County. Analysis of county general ledger accounts for fiscal year 2022 identified that the four county departments that enter into the most health and human service contracts are the Joint Office of Homeless Services, Department of County Human Services, Health Department, and Department of Community Justice. From there, we examined county general ledger accounts for fiscal year 2023 and selected a sample of 21 providers, 53 contracts, and 232 invoices for testing. We focused our testing on providers with total expenditures over $500,000, by department.

In our review, we found that providers that enter into health and human service contracts with the county can have contracts with more than one county department. To take that into consideration, we included in our sample 13 providers that contracted with one county department, four providers that contracted with two county departments, three providers that contracted with three county departments, and one provider that contracted with all four departments.

We evaluated the extent to which the county monitors health and human service contracts at the department level by asking the following questions:

- Do county departments have processes and controls in place to adequately monitor contracts to ensure contracts performance metrics are being met?

- Do county departments monitor contracts in a consistent and equitable manner across providers?

- Do county departments evaluate risk to ensure support is being applied when and where necessary?

- Do county departments have processes and controls in place to adequately review and approve provider invoicing to ensure proper payments are being made?

To accomplish the four objectives of this audit, we:

- Used Workday to analyze expenditures.

- Reviewed contract monitoring best practices from industry associations.

- Interviewed county leadership, departmental and division leadership, staff, and supervisors about contract monitoring resources and practices.

- Examined deliverables and notes related to the initiative to improve countywide contracting systems and processes.

- Verified internal controls and reviewed countywide, departmental, divisional, and/or programmatic policies, procedures, and guidance related to contract monitoring.

- Reviewed 53 contracts and 232 invoices for 21 providers and the monitoring documentation for each contract and invoice tested.

- Evaluated data across service providers for timing of payments, county support provided, and contract monitoring, risk evaluation, and consistencies in monitoring activities among and within departments, divisions, and programs.

- Surveyed the providers scoped into this audit about county contract monitoring activities and their experiences working with the county.

This population of providers and their invoices were sampled using a non-statistical sampling methodology, using data from Workday. We also reviewed copies of contracts from the county's contract management system, Jaggaer.

We assessed the reliability of data by (1) performing electronic testing for obvious errors in accuracy and completeness, (2) interviewing county officials knowledgeable about the data, (3) reviewing related documentation, and (4) worked closely with county officials to identify any data problems. We determined that the data were sufficiently reliable for the purposes of this report.

We conducted this performance audit in accordance with generally accepted government auditing standards. Those standards require that we plan and perform the audit to obtain sufficient, appropriate evidence to provide a reasonable basis for our findings and conclusions based on our audit objective. We believe that the evidence obtained provides a reasonable basis for our findings and conclusions based on our audit objectives.

Audit Staff

Michelle Greene, Management Auditor

Annamarie McNiel, Operations & Audit Director