Published January 2026

Report highlights

What we found

The Auditor’s Office follows up on audit recommendations to support county government’s accountability.

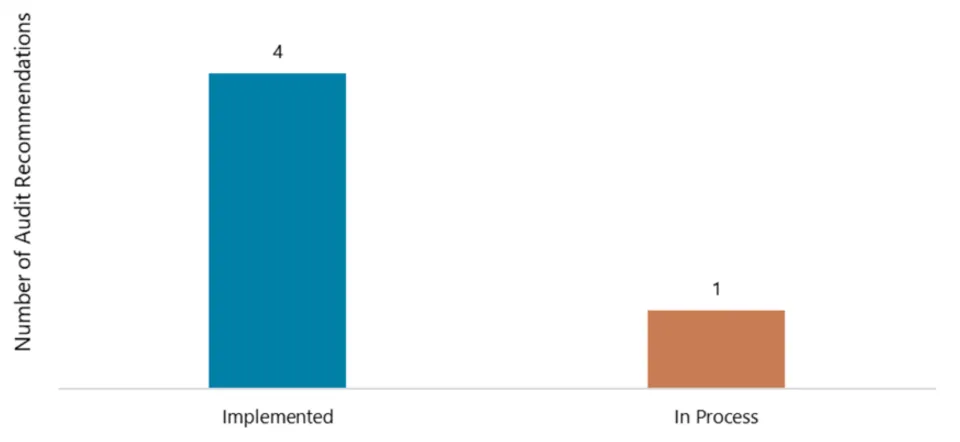

We consider the county to have implemented four of the five recommendations from our 2024 Contract monitoring audit: Consistent countywide approach needed, with one still in the process of being implemented.

What the statuses mean

- Implemented – Auditee has fully implemented, or auditee has resolved the issue to meet the recommendation’s intent.

- In Process – Auditee has started implementation.

- Not Implemented – Auditee has not implemented, or does not intend to implement.

Status of Audit Recommendations

Recommendations implemented

Recommendation #1: The Chief Operating Officer (COO) should work with departments to develop a current standard contract monitoring policy that can be used as a framework countywide.

The county established a central Contract Administration unit within the Department of County Management to implement and maintain countywide contract administration policies, procedures, standards, and training.

The Contract Administration unit did the following to develop new countywide contract monitoring standards:

- Reached out to departments to get their input for the development of the new standards.

- Provided regular status updates to employees who were identified as impacted by the new standards.

- Ran a pilot program with three departments: Health Department, Homeless Services Department (formerly Joint Office of Homeless Services), and Department of County Human Services to help inform the new standards.

- Based on the countywide input and pilot program, developed a contract administrative procedure and a contract administration standards manual and made these available on the Contract Administration unit’s county website.

- Developed training for the new standards that was made available countywide.

The Board of County Commissioners adopted a contract administration policy, which includes the contract administration manual and training, as part of the FY 2026 Financial and Budget Policies, on June 12, 2025.

Additionally, the County Chair signed a contract administrative procedure (CON-3) effective August 15, 2025. This procedure outlines the responsibility and authority for the contract administration function to be centralized in the Contract Administration unit. The procedure also outlines responsibilities for departments.

Recommendation #3: The Chief Financial Officer (CFO) should evaluate the inputs into Workday that drive an invoice’s “Due Date” to help ensure this date can be used to evaluate the county’s compliance with provider payment terms.

Central Accounts Payable (AP) worked with the County’s ERP Finance team to require an “Invoice Received Date” when an invoice is entered into the county’s enterprise resource planning (ERP) system, Workday, for processing.

Central AP communicated the definition of the “Invoice Received Date” to all department finance managers. It is the date that any Multnomah County employee or business office first receives the invoice from the supplier that is complete and accurate (e.g. can be processed for payment). This definition is also shared on Central AP’s internal website.

The “Invoice Received Date” and a calculation for the processing times are now included as part of a standard Workday report that is available to all finance staff.

The “Invoice Received Date” is still a manual entry and can therefore be entered incorrectly. We ran a report on just a few invoices and found the “Invoice Received Date” was entered incorrectly in some cases. In those cases, the date entered was the date received by the department AP unit, which was later than the date the county first received a complete and accurate invoice from the supplier. Since this issue cannot be fixed with an automated control, correcting this will require ongoing communication with AP staff to better understand and apply the “Invoice Received Date” accurately.

Central AP has been able to implement other automated controls though. This includes requiring a date in the “Invoice Received Date” field and having it be a reasonable date. For example, the system will prevent the submission of an invoice if no date is entered or if an invalid date is entered. A pop-up error message will occur and the error must be cleared before an invoice can be submitted. An example of an invalid date is a date that is more than two years prior to the current date.

Central AP is continuing conversations with departments and will provide more training at a January 2026 finance staff meeting.

We consider this recommendation to be implemented because they have responded fully to the recommendation. However, there is a need for continued training to help ensure a shared understanding of the definition of "Invoice Received Date" by those entering invoices.

Recommendation #4: The Chief Financial Officer (CFO) should develop a mechanism to evaluate department compliance with provider payment terms.

Central Accounts Payable (AP), which reports to the CFO, has developed invoice tracking tools which include:

- A Workday report, available to all departments, has been expanded to include additional data fields to help monitor invoice payment compliance.

- The Workday report now includes calculations of invoice processing times.

- A department-specific report, using the Workday report noted above, that analyzes invoice data. This report shows the percentage of invoices paid beyond their payment terms. Central AP provides this report to departments quarterly.

- A summary report provided to the County’s CFO on a quarterly and annual basis with countywide analysis to help monitor progress and compliance.

Central AP’s management told us they work with each department to discuss the results of their report and work on ongoing process improvements. Additionally, they continue to work with the ERP Finance team to make improvements in Workday to help provide more accurate data entry and increase the usefulness of the Workday report.

We consider this recommendation implemented as Central AP has developed and implemented a monitoring process that helps evaluate department compliance with provider payment terms.

Recommendation #5: The Chief Financial Officer (CFO) should develop training and information tools for both county program staff and managers and service providers so that there is consistency of information being shared. It is important that information and training are provided consistently and to those performing the contract monitoring tasks. We recommend this take the form of an annual symposium (or similar) and that it includes information sharing on:

- the tasks and expertise the CFO’s Office supports

- limitations of the CFO’s Office supports

- updates to policies, standards, and regulations impacting contract monitoring

- new or emerging issues

The County’s Fiscal Compliance unit, which reports to the CFO, has provided two trainings to county staff. The first training was held in January 2025 and was provided to contract specialists. The second was held in February 2025 and was provided to program staff. The trainings included an explanation of what the Fiscal Compliance unit does, general information about some of the contract requirements, and updates on federal guidance impacting contracts.

The Fiscal Compliance unit plans to continue to provide training to county staff on an annual basis with a focus on the program staff (versus contract specialists). From discussions with Fiscal Compliance management, the reason they will focus on program staff is that this group works directly with service providers.

While the Fiscal Compliance unit does not plan to provide direct training to service providers, management feels the trainings outlined above will provide the tools to program staff to support service providers as needed.

We consider this recommendation implemented since the Fiscal Compliance unit has provided training and information to county staff and intends to continue a training program annually with program staff.

Recommendation in process

Recommendation #2: The Chief Operating Officer (COO) should develop a mechanism to evaluate department compliance with the countywide contract monitoring policy.

Based on information shared by management, the Contract Administration unit is developing a reporting tool to collect contract deliverable data from departmental tracking systems. This reporting tool is expected to show individual contract performance in achieving contract deliverables. Due to the differing systems departments use to track deliverables, software to aggregate the deliverable information is being researched. The reporting is anticipated to be piloted by February 28, 2026.

County policy (CON-3) assigns responsibility and authority for the oversight of the contract administration function to be centralized in the Contract Administration unit, which is within the Department of County Management. This policy also includes a responsibility for the monitoring process to be performed by the Department of County Management’s Contract Administration Manager. The policy further requires departments to track contract deliverables and make them viewable for the Contract Administration unit.

We consider this recommendation in process since these efforts are still underway.

Objectives, scope, & methodology

The objectives of this evaluation were to determine the status of recommendations from the Contract monitoring audit: Consistent countywide approach needed that had a due date of June 30, 2025.

Auditors evaluated the status of recommendations based on interviews, documentation, and other available evidence.

Updating the status of a recommendation

During each audit our office conducts, we develop recommendations intended to improve government operations, particularly with regard to effectiveness, transparency, accountability, and equity. Our goal for evaluating the status of recommendations is to help ensure management implements these recommendations for improvement.

We recognize that after we publish an evaluation on the status of recommendations, management may fully implement a recommendation that we reported was in process or not implemented. Management can then provide evidence to the Auditor demonstrating why the recommendation’s status should be changed in the Auditor’s future reporting. The final decision on whether to change any recommendation’s status rests with the Auditor.

Staff

Annamarie McNiel, CPA, Operations & Audit Director